Adyen H2 2025 Earnings Review: Credibility Waning as It Enters Its “Second Act”

Adyen reported H2 2025 results yesterday, with the stock finishing down 22% on the day. Key metrics:

Transaction volume: €398.4 billion vs. €408.9 billion consensus (missed by ~3%), up 15% YoY (FX was likely a ~400 basis point headwind).

Net revenue: €672.3 million vs. €688.0 million consensus, up 15% YoY / 19% FX-neutral (missed by 2% in constant currency).

2026 revenue guidance was revised from “low-to-mid twenties” at the November investor day to 20-22% FX-neutral.

EBITDA margins are expected to be flat in 2026, largely due to the company hiring a net new 550-650 full-time employees. This represents a 12-14% YoY increase in headcount.

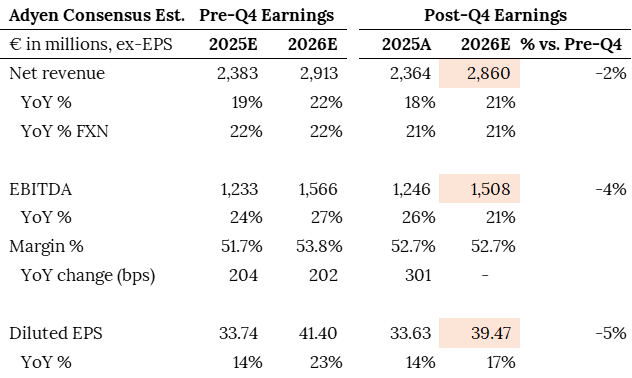

This results in 2026 consensus revenue / EBITDA / diluted EPS likely being revised down by ~2%/~4%/~5%. A few notes on highlighted cells below:

Updated revenue guidance at 20-22% likely results in consensus at best anchoring to the midpoint 21%, but with another negative surprise, the market will be skeptical Adyen can achieve this range. This is especially true for the approximately 20% targets in 2027/2028 that Adyen set three months ago at its investor day.

Updated EBITDA estimates assume margins are flat YoY, per company outlook. There could be some conservatism on margins given the company is guiding to flat margins with FTEs expected to grow 12-14%, unless wage inflation ticks up in 2026. Achieving Adyen’s 55%+ margin target by 2028 would require ~60% incremental margins in 2027/2028 assuming 20% net revenue growth vs. 53% in 2026 and 69% in 2025.

Diluted EPS is estimated to grow slower than EBITDA since interest income is ~25% of net income and, at best, is likely to be neutral to growth and would become a headwind if rates are cut further.

Sources: Adyen public filings, Bloomberg, Ottavi estimates.

This is another quarter of negative estimate revisions. I posted the following chart in my last writeup (Adyen: Its Past & (AI) Future). If we assume that consensus estimates for 2026 EPS settle around the €39.47 that I’m estimating then this is ~16% below the level after Adyen’s Q4 2024 earnings in mid-February 2025. A stock down ~49% during that period may seem extreme but consistent negative revisions can result in the multiple overshooting to the downside (as can also happen on the upside when estimates exceed expectations), especially when considering the compounding impact lower current numbers have on future estimates and lost investor credibility. And Adyen’s multiple was at a high starting point at just under 50x next-twelve-month EPS. This is before incorporating the current market backdrop that is punishing companies for earnings misses.

Source: Bloomberg

The market is grappling with whether the consistent revisions are signs of increasing competitive dynamics (like we saw with Braintree in 2023), execution issues, a more saturated market, or a management team that over-promises. I don’t believe competition is a major concern, but it’s likely a combination of the other factors. Either way, it’s evident that Adyen’s management has created credibility issues with the market. Over the past two years in most quarters there has seemingly been a reason why numbers that miss expectations should be explained away. These include, eBay share shifts, “APAC merchants” (i.e., Temu and Shein) facing de minimis tariff headwinds in the US, and losing (or more likely, removing) Cash App.

2026 was supposed to be a cleaner story with the lapping of the negative impacts from each of these, aided by a record 2025 new customer cohort (the company states a new cohort typically contributes a mid-single-digit percentage to net revenue growth in its second year). All considered, this gave management confidence to issue a 20%+ revenue guidance for 2026-2028, but with 2026 expected to be “low-to-mid-twenties.” However, just three months later, the company revised the range lower to 20-22% FX-neutral, which Adyen’s CFO attributed to better understanding customer priorities through their year-end planning conversations:

Thanks for giving me the chance to clarify, because, again, I find this important. It’s not that we’ve lowered our view of our growth for 2026. It’s that we understand where the priorities of our customers will be in a deeper way and can share that. And it’s not about shifting priorities.

It’s about understanding where the focus of our customers will be in the following year, in any given year. I can give a couple of examples where things change from year to year. One of the reasons that we’re seeing strong growth in Latin America, for instance, is not only that we’ve been investing a lot in the product over the past years and we’ve built up a great team there and we have a strong offering, but also because, as there was some geopolitical tensions, some of our international, especially retailers, shifted some of their focus more towards that market. That’s one example of where you might see a bit of a shifting priority.

But it’s not that priorities have shifted in a big way and that’s what’s led to a lowering of our view. It’s just we have a good reflection, a refined reflection of our expectations for 2026, and that’s what we share. Now, those opportunities have a balance of when they drive revenues. Some of them drive revenues more short term.

Customer plans change and the macro remains dynamic, but this seems like an unforced error that further degrades credibility further. To be fair, some of the headwinds Adyen has faced are out of its control (i.e., tariffs), but it aggressively guided again when it didn’t need to. Adyen could’ve stated that it was targeting approximately 20% revenue growth over the next three years and that it would provide a tighter range on the Q4 call, setting guidance at 20-22%, but instead introduced the preliminary range it had to walk back. In addition to the revised guidance, the market is also grappling with the fact that Adyen’s Q4 growth was already below the bottom end of this range at 19 YoY FX-neutral.

Adyen is Squarely in Act 2

Putting management communication aside, Adyen’s core Digital business — where it processes online payments for enterprise merchants — is maturing. Digital net revenue grew 5% YoY on a reported basis, 10% FX-neutral, and 11% FX-neutral excluding Cash App. Further adjusting for the APAC retailer headwinds would get Digital FX-neutral underlying revenue growth to ~13% YoY. Adyen also called out an impact from a large Digital customer migrating to Unified Commerce as it rolled out in-person payments with Adyen. It’s unclear the impact this had, but maybe a few percentage points. Digital’s underlying FX-neutral net revenue growth was in the teens throughout 2025 and that pace seems likely to persist given Adyen’s relatively high penetration of enterprise ecommerce. To achieve its ~20% revenue growth goals, Adyen will need Unified Commerce and Platforms to make up for Digital’s shortfall. It was notable that Adyen positioned Unified Commerce as one of its two differentiators in the opening page of its H2 2025 shareholder letter:

Looking ahead, two factors increasingly define our differentiation. First, Dynamic Identification adds an intelligence layer to our platform, enabling real-time decisioning that improves conversion, reduces cost, and manages risk with greater precision as our customers scale across channels. Second, our Unified Commerce offering creates a structural advantage that is difficult to replicate at scale. By connecting in-person and digital data on a single platform, we provide a complete, end-to-end view of the customer journey. Together, these capabilities position Adyen to operate where commerce is most complex and most valuable, accelerating our progress toward becoming one of the largest fintech players in the world.

This is not to say Digital won’t continue to be a meaningful driver of growth, but it seems likely Digital will be a sub-20% revenue grower going forward (and management seems to be comfortable admitting that). This requires investors to believe that Unified Commerce and Platforms, which collectively account for 46% of net revenue, can offset a likely ~teens growth rate in the more mature Digital segment. For example, if Digital grows 10-15% in 2026, Unified Commerce and Platforms would together need to grow 25-33% to achieve the low-end of Adyen’s 20-22% range. Achievable given both segments exited 2025 already there on an FX-neutral basis, but highlights Adyen is squarely in its ‘second act.’

Fortunately for Adyen, it is well positioned for both, especially Unified Commerce because 1) Adyen is uniquely differentiated as the only next-generation processor that does offline/online well at scale; 2) it allows Adyen to address the in-person payments segment of the market which is ~80% of retail sales; and 3) the installation of terminals results in stickier customer relationships and wallet-share that can approach 100% vs. 40-60% for Digital.

Other Earnings Takeaways

Some other takeaways from earnings:

AI

Adyen announced its “Personalize” launch, which is a new module within Adyen Uplift. Personalize leverages its Dynamic Identification tool and allows merchants to dynamically alter the payment experience in real-time to increase conversion and lower costs. Pilots showed up to 6% higher conversion and up to 3% lower costs. I continue to believe that Adyen’s innovation with AI should help it distance itself from legacy processors and allow it to capture incremental market share.

Competitively, I continue to believe that AI will be a net tailwind to Adyen’s business (AI-enabled Dynamic Identification and fraud tools) rather than a headwind. However, there is the “AI risk” that Stripe is capturing much of the AI volume growth currently given most AI startups are launching on Stripe. This isn’t atypical – Adyen doesn’t service startups and focuses on enterprise and historically has won customers from Stripe and others as their business scales enough to graduate to “enterprise.” But in the interim, Stripe’s growth will likely outpace Adyen which creates the narrative that Adyen is “losing” to Stripe.

Customer, Geographical, and Product Expansion

Adyen announced expansion with Uber and Starbucks. Starbucks rolled out Adyen in Europe after being introduced to Adyen through Starbucks’ local franchisee in Mexico, Alsea. This mirrors a typical wallet-share expansion I discussed in my Toast example. Ultimately, Adyen’s goal is to win the big prize: capturing an increasing share of international and eventually, domestic processing. Starbucks has more than 41,000 stores and Adyen is cited as powering 943 of them across the UK, Austria, and Switzerland in its earnings release, with the total count likely closer to 2,000 when including Alsea. Winning the other international markets and eventually, the US business is how Adyen goes from ~5% wallet share to 50%+.

Our partnership with Starbucks demonstrates how Adyen supports high-traffic environments and complex, multi-market operations where speed and reliability at the point of sale are critical. In 2025, Starbucks selected Adyen to power in-store payments across 943 stores in the UK, Austria, and Switzerland, supported by 2,375 Adyen payment terminals. This European rollout builds on an existing partnership with Alsea, Starbucks’ licensee, where Adyen already supports Starbucks’ payments in Mexico — extending a single, unified platform across regions. The transition to Adyen’s platform was executed at pace and with minimal disruption. Over 900 stores were live in just seven weeks, with up to 125 stores onboarded in a single week, all during business hours.

Adyen also called out expansion in Latin America several times. This is likely supporting TikTok Shop and Temu’s expansion into Brazil and other Latin American countries.

Lastly, issuing continued to be a bright spot in the quarter, with volumes growing 8x YoY. Adyen called out corporate travel booking platform, Navan, as a case study. Navan’s issuing growth with Adyen grew 5x YoY in H2, with further expansion cited.

In 2025, issuing reached an inflection point, with volumes growing 8x YoY as platforms embedded cards directly into their core workflows. This shift supports a wide range of operational use cases, from supplier payouts to employee expenses, while reducing reliance on external banking relationships. Growth also accelerated across capital and account products. Capital loan volume more than doubled YoY with over 80% of businesses returning for subsequent loans. Recent launches such as Fresha Capital7 and YetiPay8 extend these capabilities into vertical SaaS platforms, where fast, embedded financing directly supports business growth.

Where does Adyen go from here?

All told, I don’t believe any of these concerns are disqualifying to an investment, especially with the company positioned to grow EPS at least in the high-teens percent compounded over the next three years with the stock at 23x/19x 2026/2027 EPS and sentiment poor. The growth drivers are in place for Adyen to sustain 20%+ revenue growth and on an underlying basis (ex-one-time issues cited), Adyen’s volume growth is well into the twenties currently. Adyen remains the dominant enterprise ecommerce merchant acquirer, is well-positioned to capitalize on AI, and is uniquely positioned to capture meaningful share in Unified Commerce and Platforms, but management has credibility to restore over the coming quarters.