Adyen: Its Past & (AI) Future

Ahead of Adyen’s Q4 earnings tomorrow, I wanted to share some thoughts on Adyen especially given the recent selloff. For additional background on Adyen, I recommend reading Bob Hammel’s September 2025 post and his more recent write-up.

Revisiting Adyen’s Past

Before getting into possible future scenarios, I think it’s valuable to briefly review the past since it provides useful context on why the stock is where it is today.

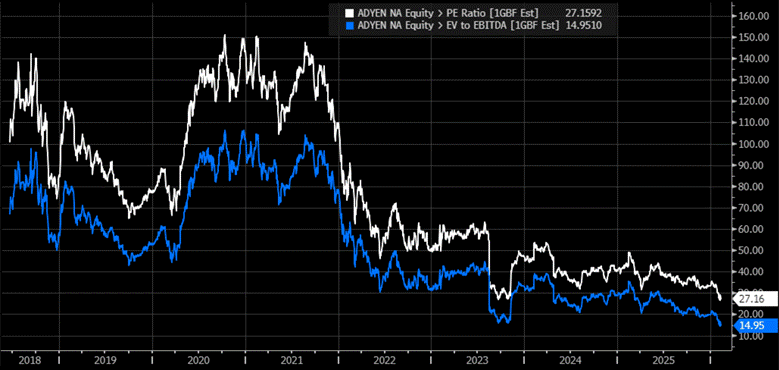

From the company’s June 2018 IPO until mid-August 2023, Adyen’s stock generated a 42% compound annual return, driven by a 36% revenue CAGR and 39% EPS CAGR.[1] The stock was rewarded for this growth and execution—its average NTM EBITDA and P/E multiples were ~65x and ~90x, respectively, during this period (Covid-era valuations also played a role).

Source: Bloomberg

Adyen’s H1 2023 earnings on August 17, 2023 changed everything. Adyen reported significantly slower than expected growth, driven by increasing competitive intensity from PayPal’s Braintree (one of Adyen’s largest US competitors). Under PayPal’s old leadership (now, old-old leadership), PayPal pivoted to use Braintree as a loss-leader in many instances to win enterprise business, with the goal of bundling PayPal’s other higher-margin products (branded checkout, Hyperwallet, etc.). This uneconomic pricing resulted in Adyen losing wallet share among several key large enterprise clients, including eBay.

Adyen was in the midst of a multi-year investment cycle, scaling its engineering and sales teams materially, and the company experienced negative operating leverage as a result of slower revenue growth. For the first time since the IPO, questions about Adyen’s advantages and longer-term growth and profitability were raised. Adyen’s stock fell 39% the day of its H1 2023 earnings.

Within a few months after the selloff, the stock recovered much of its losses as the company hosted its first investor day in November and provided a Q3 update. However, since then Adyen’s stock has been mostly range-bound, with valuation multiples in a consistent downtrend. The stock currently trades at~27x NTM earnings on consensus numbers, which is the same as Adyen’s trough earnings multiple after the H1 2023 selloff.

Source: Bloomberg

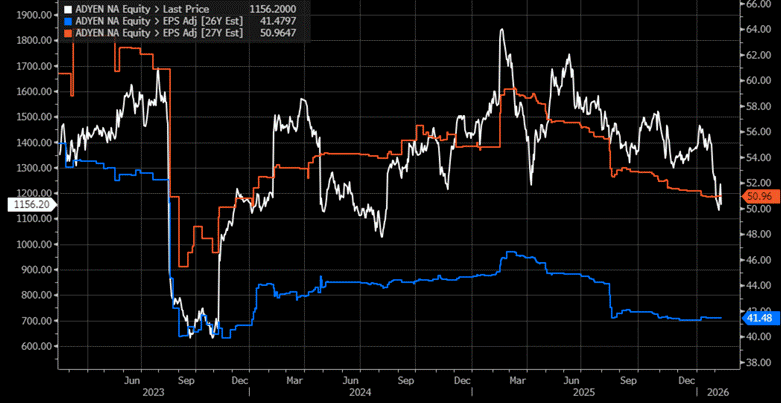

Adyen shares are down ~17% year-to-date and ~25% over the past year. This is in part due to negative earnings revisions, with 2026/2027 adjusted EBITDA and EPS all down 10-14% from the recent peak in mid-March 2025. More recently, general payments sector volatility and emerging concerns about AI disruption have sent the stock down further.

Source: Bloomberg

Unpacking an Adyen Long Thesis

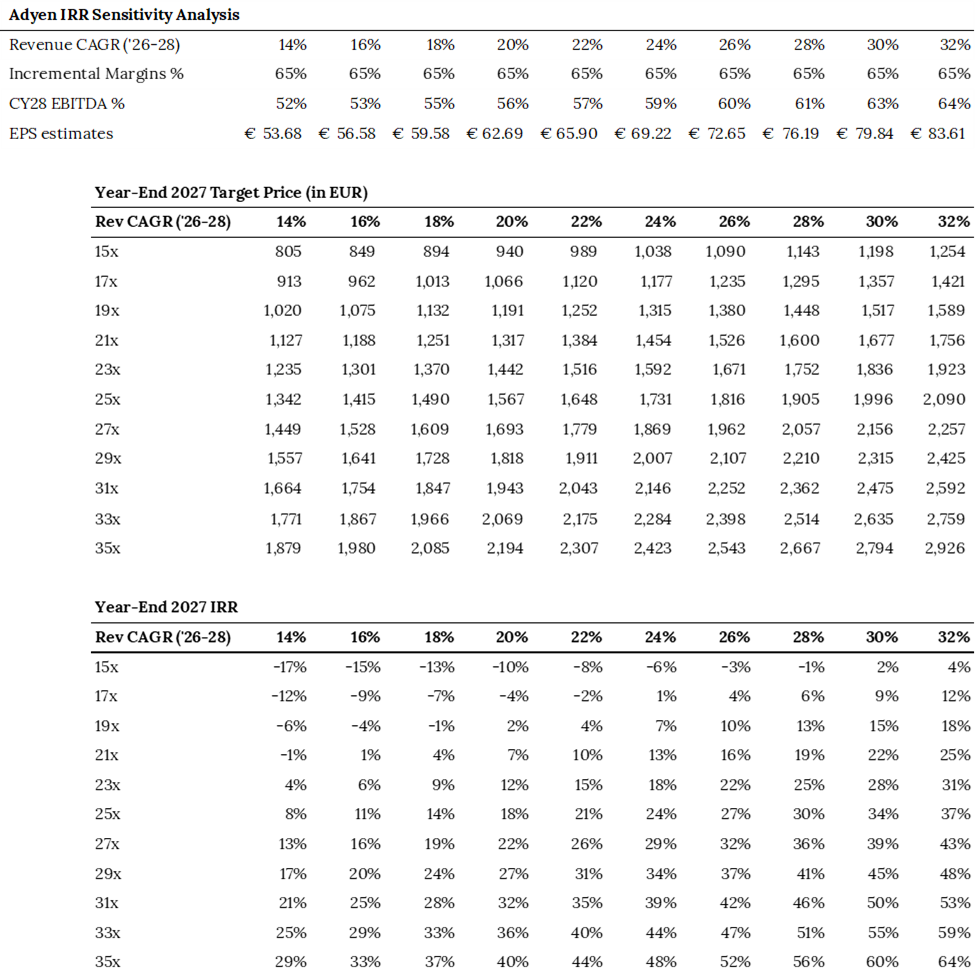

All told, the selloff has pushed Adyen to levels where the prospective returns are potentially more compelling than they have been in a while. At Adyen’s investor day in November, the company shared updated financial targets that include 2026 revenue guidance of low-to-mid twenties and for growth in 2027/2028 to be approximately 20%, with more specific guidance given annually.

Adyen increased its target EBITDA margins to 55%+ by 2028 and reaffirmed capital expenditures to 5% of net revenue, consistent with historical levels. If one believes that Adyen can achieve its guidance then the forward returns are potentially attractive, depending on the exit multiple assumed. Adyen trades at ~27x 2026 EPS for a stock that will likely compound EPS in the mid-20%s through 2028 if it achieves its guidance.

The analysis below assumes a year-end 2027 exit on 2028 numbers. The EPS estimates are informed by a few key variables, including 2026-2028 revenue CAGR and incremental EBITDA margins. All other income statement assumptions (tax rate, interest income) are in line with current trends. If one believes Adyen can compound revenue at 20-22% through 2028 then an EPS range of €62.69-65.90 is plausible. For this example, assuming 23-27x 2028E EPS would generate an IRR of 12-26% by year-end 2027. As of this writing, Adyen’s stock trades at €1,156.

Note: these assumptions are meant to be illustrative to frame the potential stock returns in different scenarios and are not a recommendation or investment advice.

Source: Adyen public filings, Ottavi estimates

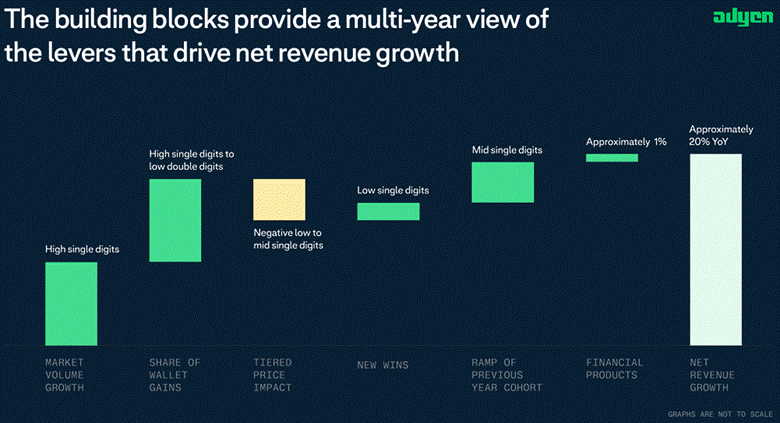

The core building blocks to achieve 20%+ revenue growth in 2026 and ~20% in 2027/2028 are predicated on ~40% from existing customer market volume growth (assuming “high-single-digits” is ~8% growth) and ~60% from new wins, expanding the wallet share of existing customers, and adoption of newer products (financial products)—offset by Adyen’s tiered pricing model.

Simplistically, for market volume growth, one can use ecommerce growth as a proxy for Adyen’s digital volume and Visa and Mastercard’s volume growth as a proxy for point-of-sale volume, which was 23% of Adyen’s total in Q3 2025. Visa and Mastercard are expected to grow volume ~9-10% in 2026, while global ecommerce is forecast to grow 7.2% in 2026.[2] A more granular analysis would examine sales trends of Adyen’s largest merchants or focus on trends in Adyen’s largest verticals, like ecommerce, luxury and food & beverage. Assuming consumption trends stay consistent, at least in 2026, Adyen’s market volume growth assumptions appear achievable, but remain subject to the macro environment.

Source: Adyen’s November 2025 investor day

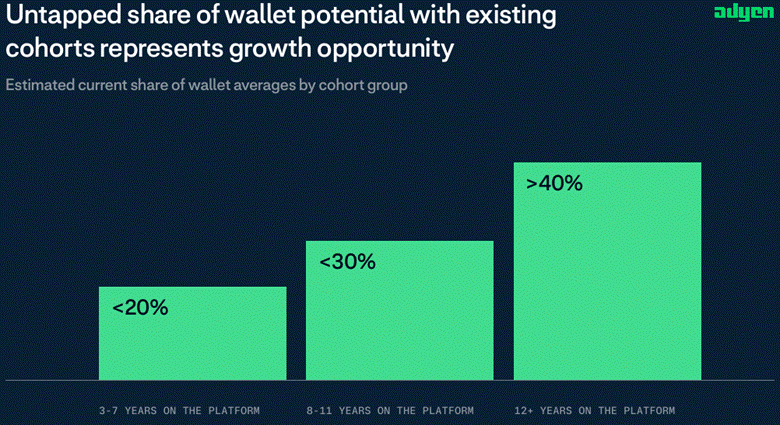

Adyen’s Wallet-Share Gains

Adyen estimates that its wallet-share for its oldest cohorts is 40%+, but still with room for expansion, while earlier cohorts can be <20%. Adyen’s wallet share can be as high as 100%, but varies depending on the merchant type and whether Adyen is processing online, offline—or both (i.e., “Unified Commerce”). Offline relationships tend to move closer to 100% over time due to the installation of hardware terminals in-store, while online is typically split between 2-3 processors, with one processor capturing the majority of the volume, while the others are leveraged for redundancy and for negotiating lower prices at renewal.

Source: Adyen’s November 2025 investor day

A typical merchant lifecycle might resemble something like this: a large multinational consumer brand based in the US with operations across the US and Europe might start processing with Adyen in the UK to test Adyen’s performance, particularly on key metrics like authorization rates. Adyen’s net take rate for this merchant processing just in the UK might be, for example, 25 basis points, but to incentivize the merchant to shift more wallet share to Adyen across other European countries and the US, Adyen will offer different pricing tiers if volume targets are achieved. If Adyen’s wallet share increases from, say, 10% for the UK-only to 50% as the merchant goes live with Adyen across all of its markets then the 25 basis-point take rate might be reduced to 15 basis points. Adyen generates more revenue per merchant and the merchant saves on per transaction costs. Adyen’s marginal costs to process an incremental transaction are nearly zero, so it will gladly exchange lower revenue per transaction for higher overall revenue and profit per merchant. Adyen’s tiered pricing and wallet share gains work hand-in-hand.

A more concrete real-world example of this dynamic is Toast. Toast uses Adyen as its acquirer in international markets (the UK, Ireland, and Canada), while it uses Worldpay and Chase in the US (process note: Toast identifies which merchant acquirers it uses in its Merchant Service Agreement for each country). Toast is likely using these international markets as a testing ground before deciding whether to expand with Adyen in the US.

It’s plausible that eventually Toast will want Adyen to be one of its two acquirers in the US and reduce the total number of global acquirers from three to two. My guess is that Worldpay would be the most at risk since Toast likely uses Chase for other banking services and has a subsidized rate. If so, Adyen’s expansion to Toast’s US business would unlock an addressable ~$200 billion in incremental payments volume.[3] In this example, Adyen likely only captures 5-10% of Toast’s volume, but there’s a defined pathway for this to increase to 50%+ over time if it becomes one of Toast’s two processors in the US.

Navigating AI

An increasingly important consideration for Adyen’s ability to retain and grow with existing customers, and win new ones, is its ability to leverage AI and adapt to the changing ecommerce landscape as agentic commerce emerges as a new sales channel. At least part of the reason for Adyen’s recent selloff is that the market is assessing whether Adyen will be a winner or loser in this new and evolving paradigm.

As I briefly highlighted in my recent post (Payments: Assessing the AI, Agentic, and Stablecoin Risks for Merchant Acquirers), the agentic debate largely comes down to whether one thinks agents will leverage the existing payment rails or use new ones (i.e., protocols using stablecoins)—and how the value chain will evolve in the payments stack within agentic commerce. My working hypothesis is that the existing rails are best positioned to win in agentic for the majority of traditional consumer purchases.

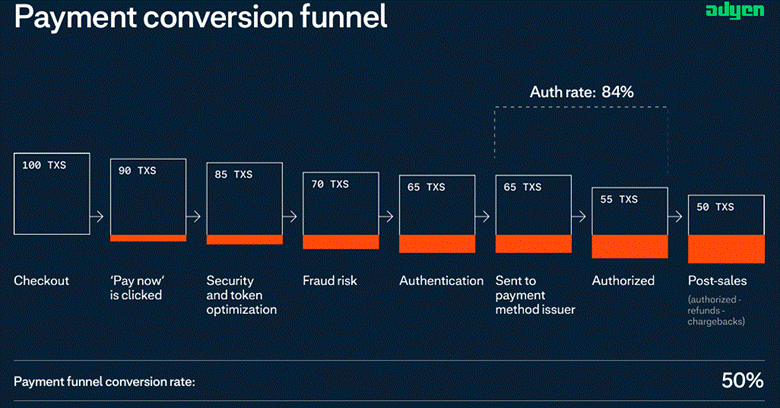

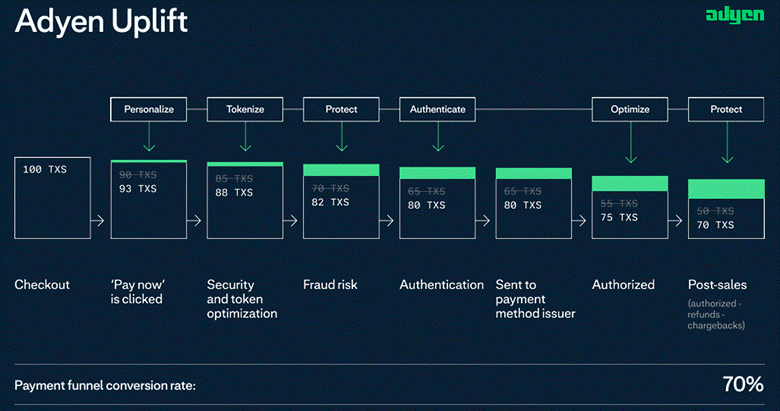

For Adyen, agentic commerce and AI are intertwined. First, ~77% of Adyen’s payment volume is transacted online, where fraud is 8x higher than in offline channels, with authorization rates 6 percentage points lower than in-person transactions.[4] With the proliferation of AI-enabled fraud by bad actors, protecting personal information, while correctly verifying legitimate transactions is arguably more challenging than ever. The most prevalent and likely use case for Adyen with AI is creating more robust fraud tools (in addition to leveraging it for more efficient internal engineering), which is where its AI-enabled product suite—Adyen Uplift—comes into play. Adyen Uplift reduces false positives by 42% and delivers conversion improvements of 1-6%.[5] Adyen is well-positioned to capitalize on AI given its single tech stack that it’s built entirely in-house—with no M&A— and its immense scale of €1.4 trillion in payments volume, with data spanning offline/online, across verticals, and geographies.

Adyen used the following example to show the type of results conversion increases from Adyen Uplift at the company’s November 2025 investor day:

Source: Adyen’s November 2025 investor day

Agentic Commerce Increasing Payments Complexity

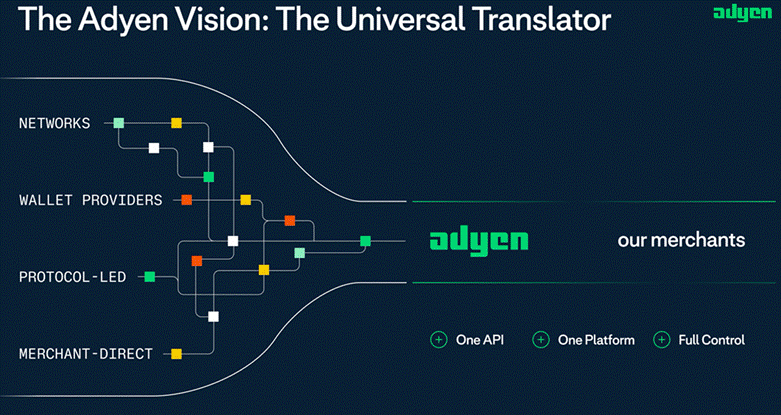

The agentic landscape is quickly evolving, including which standard will help govern agentic economics, roles, and rules. Google’s Universal Commerce Protocol (UCP) and OpenAI’s Agentic Commerce Protocol (ACP) are two protocols jockeying to set the industry’s standards. Ultimately, for Adyen, this increasing complexity and commerce fragmentation should be a net benefit that reinforces its value proposition as it integrates with all the different payment modalities and enables merchants to focus more on what they do best. Merchants want to minimize the number of processors it uses and will favor those that reduce complexity in selling across channels.

Adyen framed this in their November 2025 investor day as being “the universal translator”:

So in this new ecosystem, we see Adyen as a universal translator for agentic commerce. We see this as the bridge for merchants to be able to manage and process any payment they want through any AI protocol, through any AI agents. One API, one platform, full control. And this isn’t just about payments. It’s about data integrity. It’s about trust. It’s about identity. When you combine all these three things together, it’s not about this one-off transaction. It’s about loyalty with that customer. And so while others are focusing on single components, authentication discovery, we’re focusing on the [rails] that pull all these components together in a seamless fashion for our merchants.

Source: Adyen’s November 2025 investor day

In the US, there has been a valid argument over the past several years that merchant acquiring in ecommerce was becoming commoditized, particularly since most online purchases run on Visa and Mastercard rails. However, agentic commerce could reverse—or at least slow—this trend, as payments become increasingly complex.

Either way, the application of AI and enabling agentic commerce should allow Adyen (and Stripe) to further distance themselves from legacy providers who cannot innovate fast enough to meet the increasing demands from merchants. For Adyen, this should at the very least be supportive of its wallet-share gains and new wins assumed in its mid-term targets and could even accelerate momentum.

[1] Adyen; revenue and EPS CAGRs are from 2018-2023.

[2] Bloomberg, Shopify, eMarketer.

[3] Bloomberg consensus estimates for Toast payment volume in 2026 is $232 billion, with majority from domestic.

[4] Visa’s Global Product Drop. April 04, 2025.

[5] Adyen

That’s where it gets interesting.

The story still sounds clean—growth, margins, AI as a tailwind.

But that’s also what the setup looked like before the break.

The question isn’t whether Adyen can execute.

It’s what has to stay true for the return to work from here—and how much room there is if any part of that shifts.

The risk isn’t failure.

It’s the story holding… and the outcome still disappointing.