Crypto's Dot-Com Moment? 2000 Parallels and the Coming Inflection Point

Santiago R. Santos (@santiagoroel on X) wrote an insightful Substack post titled ‘The Most Uncomfortable Phase of Crypto Has Begun.’ In his writeup, he argues that crypto adoption is accelerating, but prices may fail to keep pace, lagging behind the technology’s proliferation. He analogizes this to the Dot-Com bust in the early 2000s, when the Nasdaq fell 78% peak-to-trough from March 2000 to October 2002 and stock valuations lagged the internet adoption.

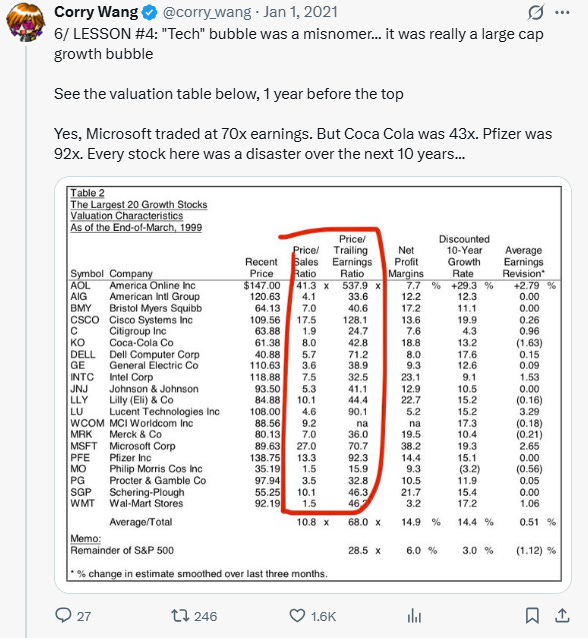

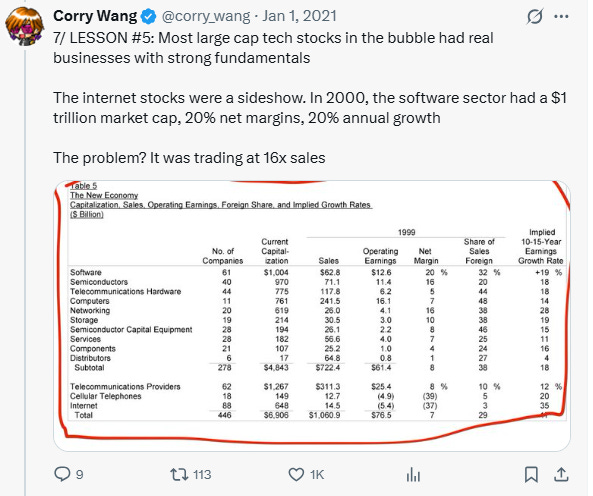

First, I believe some clarifications about the Dot-Com bubble are required, which provide useful context. Corry Wang (@corry_wang on X) had a great thread on this topic back in Jan 2021. This was posted in the throes of the Covid Tech bubble, but is as relevant today. The entire thread is worth reading, but his findings that are most relevant to this post:

The Dot-Com era was largely a large-cap growth bubble—not an Internet stock bubble.

The ‘Internet’ subcomponent of Bernstein’s (Wang’s former employer) ‘New Economy’ categorization was only $648 billion, or less than 10% of the New Economy’s total capitalization and about 4% of the total market. Internet fads like Webvan receive considerable attention, but these companies were only a small part of the story. Software and companies related to the telecom/fiber buildout accounted for much of New Economy’s market cap.

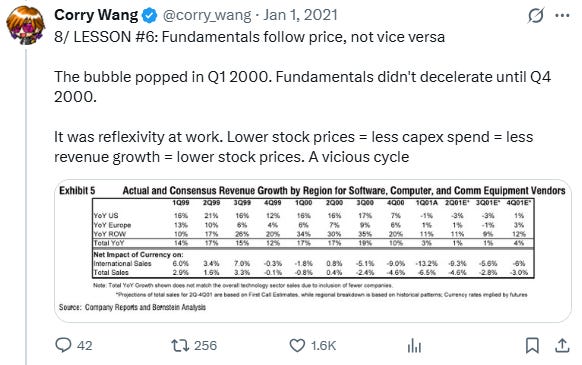

Reflexivity was real, but on a lag.

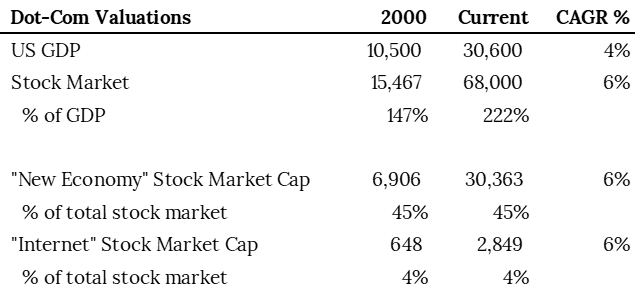

With this in mind, what’s the relevance to current crypto markets? For starters, crypto’s market cap in today’s terms is similar to the Internet’s market cap back in 2000—around $3 trillion.

Here’s the math: Since 2000, US GDP has compounded at about 4%, while the total market cap of US equities has grown at roughly a 6% CAGR. This corresponds to a US GDP of $30.6 trillion and a U.S. stock market capitalization of approximately $68 trillion. If we assume that the ‘New Economy’ and ‘Internet’ market caps grew at the same rate as the overall stock market, their total values would be $30.4 trillion and $2.8 trillion, respectively—the latter of which is a close approximation to crypto’s widely cited market cap figure.

Sources: Corry Wang, Bernstein, Federal Reserve, Ottavi

‘Internet’ in today’s terms is more meant figuratively to encapsulate the market cap of an emerging theme rather than Internet companies themselves, which are obviously worth much more than $2.8 trillion today.

Additionally, I think it’s a fair assumption that most would view the companies in today’s ‘New Economy’ basket as those benefiting from AI, not crypto. I forget the exact statistic I saw recently, but it put the percentage of the US stock market that benefits from AI at levels similar to the 45% estimated for the ‘New Economy’ back in 2000 (I can’t find the source, so take this with a grain of salt since this may be inaccurate). This includes semis, hyperscalers, infrastructure, energy, and so on. Ultimately, AI is increasingly prominent among investors and in the market. However, AI isn’t the purpose of this post... back to crypto.

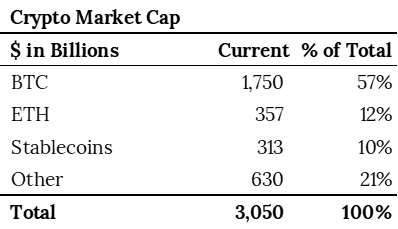

Coincidentally or not, the ‘Internet’ market cap of $2.8 trillion in today’s dollars closely matches the total crypto market cap of $3.1 trillion. This includes Bitcoin at about $1.8 trillion, Ethereum at roughly $357 billion, and stablecoins at $313 billion. Approximately 79% of crypto’s total market cap is concentrated in BTC, ETH, and stablecoins, with the remaining 21% held by all other crypto, including altcoins and tokens.

Sources: CoinGecko, Ottavi

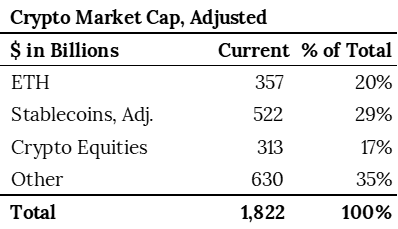

However, crypto’s market cap is apples-to-oranges with the Internet’s market cap back during Dot-Com. Firstly, BTC accounts for 57% of crypto’s total market cap, but has solidified a position as a “digital gold”—and therefore, a commodity—rather than equity so should be removed from this calculation (however, the market caps of publicly traded BTC miners who generate revenue and earnings from these activities are included in “Crypto Equities”). Ethereum is included given its infrastructure generates revenue and the value of ETH is tied to this financial activity.

Instead of using the current value of stablecoins, which are tokenized treasuries not equities, it would be more comparable to include the market cap of stablecoin issuers who generate their revenue and free cash flow from stablecoins. Here, the current value of stablecoins would be ~$522 billion versus the $313 billion stablecoins in circulation. This assumes Tether’s recent $500 billion private valuation is correct (for this purpose, we’ll assume it is) and Circle’s (CRCL) publicly traded market cap of ~$22 billion. Tether’s USDT and CRCL’s USDC dominate the global stablecoin market, accounting for ~84% of the stablecoin market cap. Even assuming Tether’s $500 billion valuation is accurate, including the entirety in this calculation may be too generous given that much of Tether’s value is in its USDT stablecoin, which is not GENIUS Act-compliant (we’ll need to see how its GENIUS Act-compliant USAT scales). Still, for now, I’m including Tether in this calculation. As such, the combined market cap of $522 billion for both is a good proxy for the current stablecoin equity market cap.

Additionally, if we assumed market caps for other publicly listed crypto stocks (Coinbase, Figure, Galaxy, Bullish, the DATs including MSTR, and even Robinhood), we would arrive at another ~$310 billion in value. In total, even including all other altcoins in this figure, this would put the “true” crypto market cap at ~$1.8 trillion and well below the $3.1 trillion commonly cited – or ~2.7% of the total US stock market vs. ~4% for ‘Internet’ market cap in 2000.

Sources: CoinGecko, Bloomberg, Ottavi

Ultimately, no matter how you slice it, I think the takeaways are similar:

Crypto’s market cap is still relatively small when compared to other asset classes at ~$1.8-3.1 trillion.

From a market sense, crypto still is very much BTC and until the market cap from non-BTC eclipses BTC, many market participants will view BTC and crypto’s success as interchangeable with each other.

… and since BTC is the majority of the crypto market, other crypto assets tend to be correlated with BTC. Not helping matters are some of the marquee publicly traded crypto champions (e.g., COIN) generate the majority of their revenue and profit from trading crypto like BTC.

This also creates a dynamic in which BTC prices can induce reflexivity across cryptocurrencies. Like Wang’s observation that reflexivity was at play with software and could be at play with crypto—at least the way the industry is currently constructed where crypto asset values—or one’s views of how the industry is doing—is tied to Bitcoin’s price action.

Additionally, if we compare the recent price action in crypto, it fails to match up to Dot-Com. BTC is down ~29% from its year-to-date high, but only down 8% year-to-date and up 100%+ over the past two years. Furthermore, the market cap of “altcoins,” which CoinGecko defines as everything ex-BTC is only down 15% year-to-date and 24% when we exclude the rise in stablecoins, which are up 48% year-to-date. There is undoubtedly pain beneath the surface in many tokens and memecoins, but overall, the market is down, especially when compared to the stock market, but far from Dot-Com levels of pain. Although, much of this value destruction gets the bulk of the focus.

This highlights an important aspect regarding the current dynamic in crypto. Much of the value creation to-date has been in a “store of value” asset in BTC, for crypto to get past being more of a trading instrument to entities with enduring free cash flows, it needs to be leveraged as infrastructure to create better, faster, cheaper products and services. Potentially, the rise in stablecoin market cap growth this year while coins decline is a healthy indicator if stablecoins and other blockchain-based infrastructure can result in better real-world use cases.

Santos made this point in his post:

I think in probabilities. My highest-confidence view is that most businesses adopt crypto over the next 15 years to remain competitive. When that happens, crypto exceeds $10 trillion in aggregate value. Stablecoins, tokenization, users, and on-chain activity will grow exponentially. At the same time, valuations will reset. Large incumbents will fall. Business models that never made sense will be exposed.

This is healthy. It is necessary.

Crypto should become invisible. The more a company makes crypto the product, the more fragile it becomes. The durable winners will bury it inside workflows, payments, and balance sheets. Users should not notice crypto itself but feel the impact of faster settlement, lower costs, and fewer intermediaries.

Crypto should be boring.

The era of airdrops, subsidized demand, broken incentive loops, and hyper-financialization is ending, as it always does when capital tightens.

So, what about crypto’s future?

While this outlook may seem pessimistic, I believe crypto stands at an inflection point. Regulatory clarity—the GENIUS Act passed, CLARITY Act slated for early 2026—paired with stablecoins as superior rails for certain use cases (cheaper, faster, better) has accelerated institutional adoption. It’s early, but adoption is happening and will likely accelerate.

SEC Chairman Paul Atkins recently forecasted much of finance moving onchain in the next few years. This aligns with BlackRock’s Larry Fink and Rob Goldstein’s op-ed in The Economist touting tokenization’s potential to revolutionize finance, alongside traditional firms pledging—and investing—capital in this onchain shift (e.g. ICE’s $2 billion stake in Polymarket).

Blockchain is on the cusp of enabling superior products and redesigning financial infrastructure. Amid coin-centric focus, now is ideal to spot firms leveraging blockchain to create fundamentally superior products and services. Incumbents will adapt and thrive or get disrupted; challengers will win or lose. Ultimately, it will come down to what determines long-term fundamental value—creating superior products and services that produce enduring revenues and cash flows.

Revisiting ecommerce: Myriad players drove global penetration to 20%+ today, fueling trillions in annual sales. Financial services—similarly, a tens-of-trillions market globally—could follow suit. If blockchain achieves comparable adoption by 2050 through superior solutions, it could unlock trillions in equity value. Ecommerce birthed Amazon and other category winners while also helping presumed losers like Walmart continue to grow (now trading at a higher P/E than the disruptor). If this roadmap holds, we’re in the nascent stages of more enduring value creation via blockchain commercialization. Exciting times ahead.