Figure (FIGR), Part 1: Building the Fannie Mae & Freddie Mac of Non-Qualified Lending

What is Figure?

Figure Technology Solutions (ticker: FIGR), hereafter referred to as “Figure,” is a company disrupting the non-qualified mortgage market through its blockchain-based solutions, with nascent expansion into the broader credit and equity markets. Figure sits at the forefront of the tokenization trend, which could see trillions of dollars of assets move on-chain over the coming years.

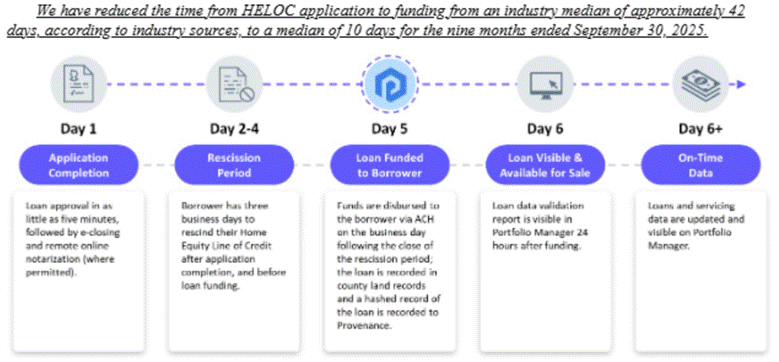

No matter the asset class, there are commonalities in Figure’s approach: use vertical integration and blockchain to reduce costs through automation and disintermediation, while scaling transactional liquidity. In HELOC, Figure in-housed the loan origination system, appraisals, and lien registry, while automating income verification and providing e-close capabilities. This reduced the origination process from 40+ days to a median of 10 days, while cutting origination costs 90%+ versus the average mortgage process.[1]

Typically, Figure demonstrates proof of concept by being its own first “customer.” In HELOCs, for example, Figure spent years originating mortgages on its own balance sheet before allowing partners to white-label its technology and originate their own branded mortgages using Figure’s loan origination system (LOS). The company is doing the same with its On-chain Public Equity Network (OPEN) by launching a tokenized version of its stock natively on-chain that is fungible with its NASDAQ-listed security.

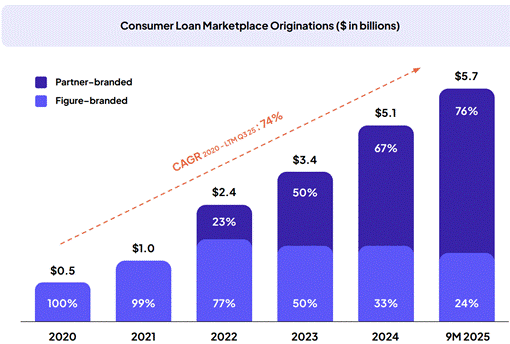

As of Q3, Figure had 246 origination partners, up 46% sequentially, and 118% year-over-year, with partner-branded origination volume accounting for 76% of total Consumer Loan Marketplace Volume for the trailing-nine-months—either through white-labeling Figure’s technology and/or selling mortgages on Figure Connect (the company’s transaction marketplace where originators and investors can buy and sell loans), or both.

Source: Figure’s Q3 2025 earnings presentation

Ultimately, the goal is to turn Figure Connect into a “TBA market” equivalent, providing the non-qualified mortgage (non-QM) market a liquid secondary market akin to what Fannie Mae and Freddie Mac offer for qualified mortgages (QM). Figure also recently started scaling several adjacent and interrelated businesses. Democratized Prime is Figure’s blockchain-based competitor to traditional prime brokerage and overnight funding markets, which will be a critical component to its end-to-end mortgage marketplace. OPEN aims to capitalize on the stock tokenization still in its infancy, but is positioned to grow substantially, especially once the crypto market structure legislation is passed. YLDS, Figure’s fixed-income security that combines the protections of a stablecoin but can pay yield (SOFR minus 35 basis points), has shown initial signs of scaling, with its in-circulation market cap growing from $21 million in November to $369 million currently.[2]

Figure’s net take rate has averaged approximately 6% of Consumer Loan Marketplace Volume, comprising:

● Ecosystem fee: ~3% on mortgages originated through the platform

● Gain-on-sale: Margin captured when mortgages are sold to investors

● Partner fees: Ecosystem and technology fees from origination partners

● Securitization fee: 40 basis points on mortgages Figure securitizes

● Servicing fee: 25 basis points on mortgages Figure services

Figure also earns interest income on cash and other liquid assets. For Democratized Prime, Figure charges 50 basis points annually on total assets.

Even with its nascent businesses providing little financial impact today, Figure’s core HELOC business is scaling fast—and profitably. In 2025, the company generated $8.4 billion in Consumer Loan Marketplace Volume, up 63% year-over-year. The company also pre-announced Q4 results on January 12, showing Consumer Loan Marketplace Volume further accelerated to 131% year-over-year, up from 40% in Q2 and 70% Q3. This acceleration reflects both growth in origination volumes and scaling Figure Connect, which accounted for 46% of Figure’s total Consumer Loan Marketplace Volume after launching in June 2024. Consensus estimates expect Figure to generate $694 million in revenue in 2026, up 36% versus 2025, and $364 million in adjusted EBITDA, up 48%.[3] The company’s expected adjusted EBITDA margin of 52% demonstrates the scalability of its model. The stock trades at ~23x 2026 EBITDA and ~42x 2026 earnings. In a future post, I’ll outline the financial details of an investment thesis, including detailing why I believe consensus estimates are conservative.

Figure was co-founded by Mike Cagney and June Ou. Cagney currently serves as Figure’s Executive Chairman and focuses on bigger picture strategic initiatives, while CEO Michael Tannenbaum oversees the company’s day-to-day operations. Cagney and Tannenbaum first worked together at SoFi, where Cagney was CEO and Tannenbaum was CRO.

The US Mortgage Market

The US mortgage market originated approximately $1.8 trillion of loans in 2025, divided into two broad categories: Qualified Mortgages (QM) and Non-Qualified Mortgages (non-QM). QMs are loans the US federal government guarantees through government-sponsored entities (GSEs) Fannie Mae and Freddie Mac. To qualify—or “conform”— mortgages must meet certain criteria established by the government. In 2024, ~95% of mortgage originations were QM with non-QM making up the remainder. Non-QM’s share has increased from nearly zero a decade ago.[4]

For 2026, the FHFA (Federal Housing Finance Agency) raised the baseline conforming loan limit for one-unit properties to $832,750, up from $806,500 in 2025 (a 3.3% increase). In high-cost areas, the ceiling can reach $1,249,125. Additional conforming requirements include minimum credit scores, debt-to-income ratios, and loan-to-value levels. Loans that fall outside these parameters are classified as non-qualified. Common examples include jumbo loans (those exceeding the conforming limit), debt-service-coverage-ratio (DSCR) loans (common for investment properties), and bank-statement loans (typically used by self-employed borrowers). The non-QM market is where Figure competes today.

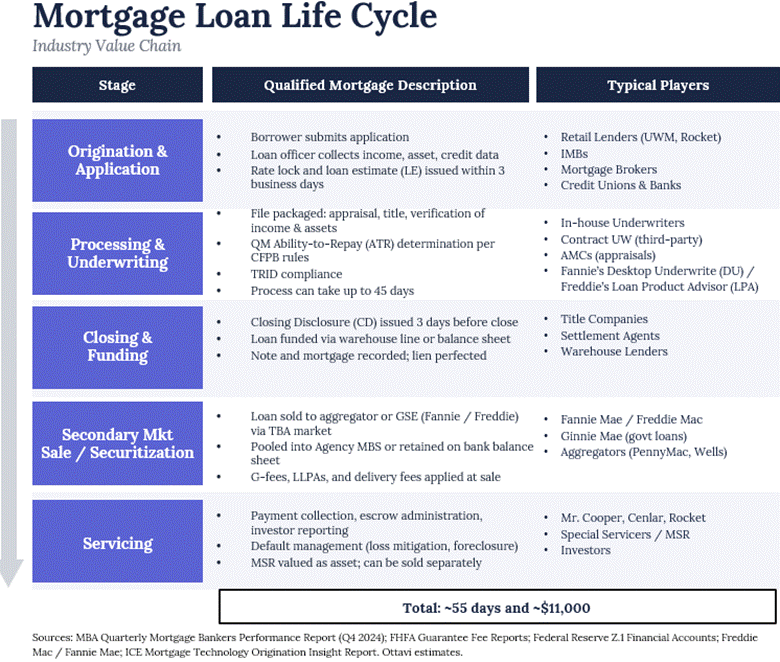

The typical mortgage process takes 55+ days to complete, including over 40 days to originate the mortgage and approximately ~15 additional days to sell the loan into the secondary market.[5] The mortgage process looks something like this:

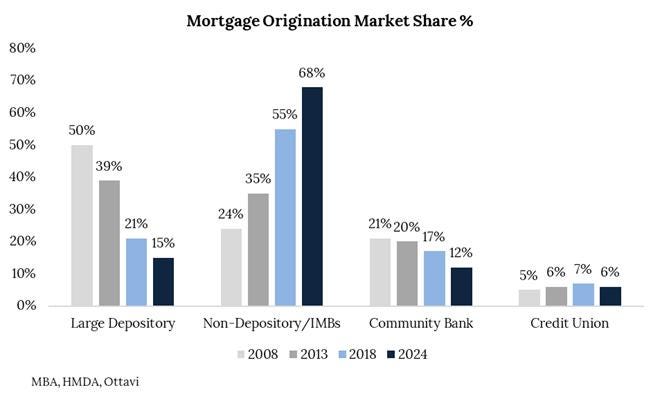

Much of the US mortgage market volume is originated by independent mortgage banks (IMBs). In 2024, IMBs originated over $1.2 trillion in mortgages, accounting for 68% of the $1.8 trillion total. This is up materially from 24% in 2008 and 55% in 2018 as large banks have pulled back on their mortgage practices. However, most of the loans IMBs originate are first-lien. Their share of subordinate loans—which include HELOCs and other non-qualified products—was significantly lower at 16%.[6] This is due to the challenging origination economics for non-QM and a lack of a secondary market. This gets to the heart of what Figure’s addressing.

Funding & Warehouse Lines

Because IMBs are not depository institutions—and therefore do not have the same low-cost deposit funding that banks enjoy—they do not retain mortgages once originated and instead, sell them into the secondary market. Without access to deposits, IMBs enter into “warehouse lines” with financial institutions to fund the gap between when a mortgage is originated and when it’s sold in the secondary market. This warehousing period averages ~15 days but can extend to several weeks.[7]

Without retaining loans, IMBs and other originators that sell mortgages are in the business of capital turnover—maximizing how quickly they can originate, close, and sell a loan to achieve unit profitability. Since revenue is largely defined by the mortgage size, interest rate, and credit quality, the objective centers on minimizing costs. Traditionally, this means leveraging technology to automate and reduce operating costs, increasing throughput to generate operating leverage, and reducing variable costs tied to time—specifically, personnel overhead, warehouse expenses, and the opportunity cost of capital being tied up in a warehouse line rather than originating additional loans.

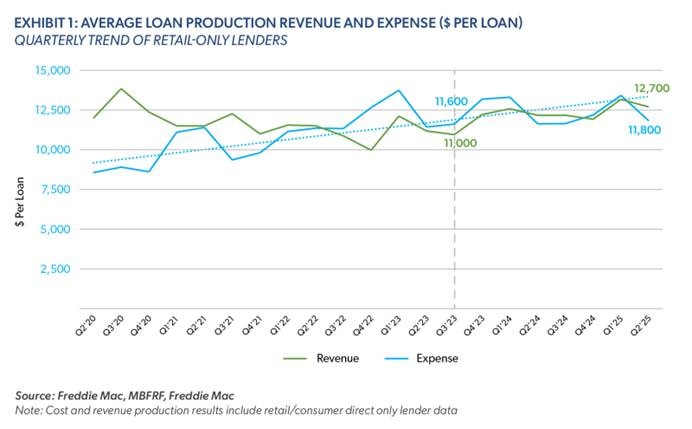

Rising Origination Costs

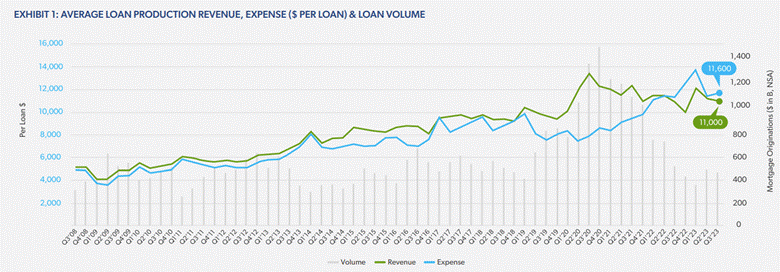

Complicating this calculus is the rising costs of mortgage originations. For roughly a decade post-GFC, originators’ average per loan revenue and expenses moved in relative lock-step even as mortgages remained a relatively low-margin product (typically a single-digit net margin).

Source: Freddie Mac

However, the pandemic disrupted unit economics. Initially, originators experienced massive economies of scale as an explosion in origination volumes spread fixed costs over more loans and a higher mix of refinancing activity which tends to have better unit profitability boosted margins. However, as volumes receded, originators struggled to maintain unit profitability, as operating leverage reversed and cost inflation continued to persist.

Much of the time and expense is due to mortgages still being a human-led process, with ~67% of per origination cost from personnel expenses (i.e., underwriting and processing). This is in part due to the processes required by Fannie and Freddie that results in human-aided documentation collection and verification. Furthermore, industry estimates showed that technology-related expenses increased from 2% per loan in 2021 to 4% in 2024.[8]

This results in many mortgage originators not generating sustainable profitability. The Mortgage Bankers Association (MBA) estimates that, on average, originators <$400 million in annual volume lose ~$1,000 per loan originated. This cohort of ~4,000 institutions originates ~$230 billion in annual mortgage volume—or ~13% of total industry volume. IMBs, on average, generated eight straight quarters of net production losses from Q2 2022—Q1 2024.[9] Even in good times, net margins are typically in the single-digits.

The TBA Market: The Lifeblood of the Mortgage Market

Once a mortgage is originated, it typically enters a warehouse line and is then sold in the secondary market. The secondary mortgage market is the lifeblood that allows the US mortgage system function. Loans are typically sold to GSEs Fannie Mae and Freddie Mac in the To-Be-Announced (TBA) market, which provide a guarantee in exchange for originators adhering to conforming guidelines. Beyond the guarantee, the market’s standardization enhances transactional liquidity. When including origination volumes transacted and other secondary transactions, the TBA market facilitates $250-300 billion in daily trading volume—many multiples the active mortgages outstanding on an annual basis.[10]

Gain-on-sale revenue also generates the majority of the origination revenue—typically 70–80% of the total—while origination fees charged to the borrower (including origination, processing, underwriting, and administrative fees) are typically ~10–20%, with warehouse net income making up the remainder.[11] Warehouse net income represents the spread between interest earned while holding the mortgage and the cost of the warehouse facility. The time to sell a mortgage, or “dwell time,” can extend up to 60 days. In total, an originator can generate revenue amounting to ~300bps of the mortgage amount.

While TBA liquidity is dependable, the process still has inefficiencies. The typical mortgage can spend at least 15 days in the warehouse facility as it goes through the necessary documentation and approval process. This ties up capital, although the incremental interest cost is generally offset by the positive carry from the mortgage’s higher coupon relative to the borrowing rate. An originator that generates $800 in profit per loan can generate 3x the amount of total annual profit by cutting dwell time from 15 days (TBA) to 5 days (Figure). This excludes the additional operating leverage from higher volume turnover.

Figure’s Disruption Begins with an Underserved Market: HELOCs

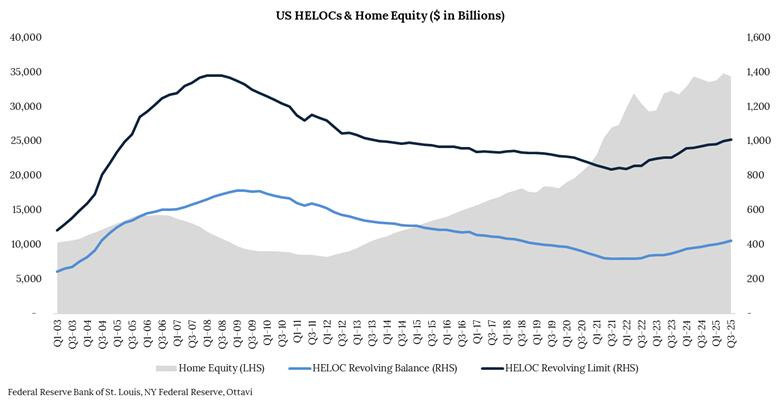

HELOCs gained notoriety during the GFC as debt balances expanded due to lax underwriting standards, including practices that allowed homeowners to use HELOCs to “piggyback” their existing mortgages—in many cases, to avoid paying private mortgage insurance (PMI) by increasing the down payment amount to the 80% threshold. Following the GFC, HELOC origination volumes declined materially as both bank and non-bank originators pulled back.

Underwriting standards are more stringent today. When used prudently, HELOCs allow homeowners to tap into their home’s equity to pay for renovations, other expenses, or simply to have a revolving credit line available. After more than a decade of consistent decline, HELOCs started to grow again in 2021 as a way for homeowners “locked in” at low mortgage rates to tap into their equity, which is at an all-time high of $34+ trillion in the aggregate.

In Q4, HELOC balances amounted to $422 billion, up 9% year-over-year—amounting to 1.2% of total home equity versus 7.9% at the peak during the GFC and 1.0% at the nadir in Q2 2022.

Figure started with HELOCs because (1) it was an underserved segment of the mortgage market; (2) it could be meaningfully improved through vertical integration and blockchain; and (3) it provided a wedge to build Figure Connect. Additionally, Figure hypothesized that it could create an application and origination process for HELOCs that rivaled that of personal loans—leveraging co-founder Mike Cagney’s experience from SoFi. The result was a process that reduced the median application timeline to 10 days vs. the typical mortgage of 42 days, and cut total origination costs to ~$750.

Source: Figure’s S-1

Beyond the demand-side pull from a significantly better origination process, Figure attracted origination partners because it allowed them to tap into a market that was largely unavailable to them due to suboptimal unit economics. Revenue generated per HELOC originated tends to be lower than for a primary mortgage, largely due to smaller average loan amounts. Using rough numbers and assuming average revenue per originated mortgage of ~300bps: a $100,000 HELOC will generate ~$3,000 in revenue versus ~$12,000 for a $400,000 primary mortgage.

While per-loan operating expenses may be lower—particularly when the HELOC borrower is an existing bank customer—the low revenue base makes it difficult to generate profits without a largely automated process. If the average personnel costs are ~67% of average mortgage’s origination costs—or $7,900—then originators would need to cut this expense by 62% just to get to break-even (assuming the originator could eliminate all other costs). This is a tall—and unlikely—task for nearly all originators.

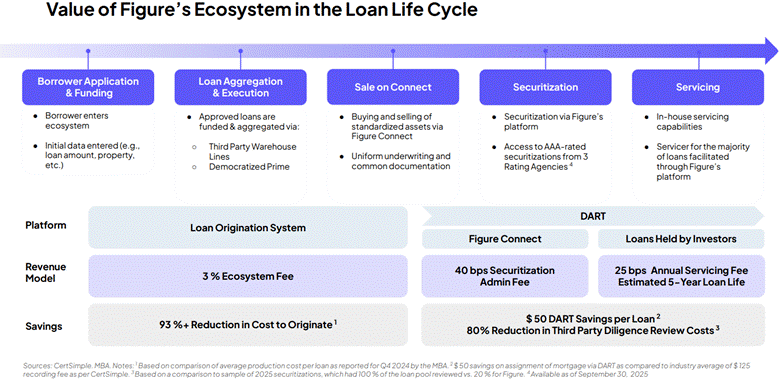

Figure Connect: Creating the “TBA Market” of Non-Qualified Mortgages

Even if an originator can make the unit economics viable, the lack of a standardized secondary market for non-QMs further compounds the challenge, making loan disposition more difficult and costly. This is why post-GFC, most HELOCs—and subordinate loans generally—are originated by depository institutions that can leverage HELOCs as customer retention tools rather than profitable standalone products. Unsurprisingly, IMBs only account for 16% of subordinate mortgages versus 68% for total originations. Figure’s value proposition has attracted 246 origination partners—and accelerating. This includes ten out of the twenty largest IMBs. Figure’s HELOC market share among IMBs reached an estimated 19% in 2025, up from 13% in 2024. However, its total market share remains relatively low at 4% of the total market.[12]

Convincing origination partners to adopt Figure’s white-labeled solution was a critical first step, but insufficient for Figure to ultimately create an end-to-end process that rivaled Fannie and Freddie for non-QM. To do so required creating a liquid, standardized marketplace where originators could seamlessly transact with mortgage buyers, which is where Figure Connect comes into play.

Figure Connect allows partners who originate using Figure’s LOS to sell their loans to investors. To create a similar guarantee mechanism, Figure launched a joint venture with Sixth Street that would act as a “guarantor vehicle”—giving originators confidence they could sell originated loans. Figure also paired Connect with Democratized Prime, allowing partners to replace traditional warehouse lines with bilateral, direct connections to lenders.

As it did with the origination process, Figure leveraged vertical integration and blockchain technology to eliminate intermediaries and cut costs. The advantages show up in a few key areas:

Bringing the homogeneity of QM to Non-QM: Figure’s LOS process produces anonymized data that lives on the blockchain. Critically, Figure’s Digital Asset Registration Technologies (DART) displaces the traditionally used Mortgage Electronic Registration Systems (MERS). DART “listens” to a transaction when consummated on Provenance—the L1 blockchain Figure uses (and which it owns ~25% of Provenance’s outstanding HASH tokens)—updating the registry in real-time. This eliminates the paper documentation process of MERS and ensures there’s no double-pledging of loans. The typical QM can have a defect rate in the mid-to-high-single-digits.[13] Figure reduces this to zero.

Reduction in third-party review costs: Figure estimates saves 80% of securitization costs because its loan data is immutably stored on the Provenance blockchain. Compared to standard securitizations in which ratings agencies may review 100% of originated loans, leveraging the blockchain reduces this to a sampling of only 20% for Figure’s AAA-rated securitizations.

Faster time to payout: Figure reduces settlement time to ~5 days versus 15+ days for Fannie and Freddie, and potentially significantly longer for private non-QM purchases. This increases volume turnover.

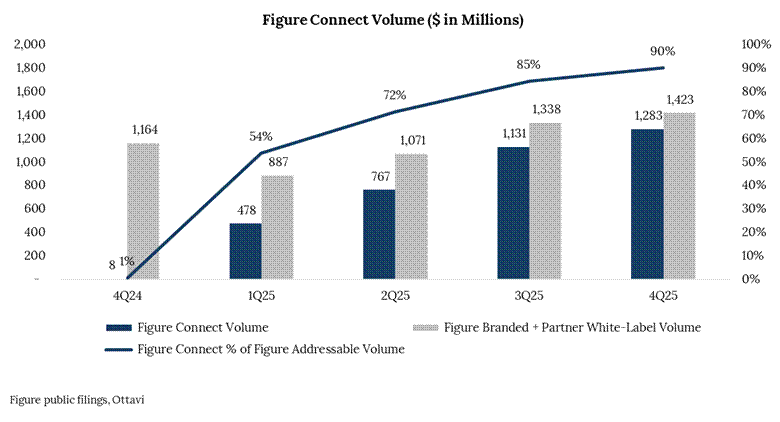

Since launching in June 2024, Figure Connect has scaled from near zero to ~90% of total Figure addressable volume (Figure-branded and Figure partner volume) within a year. This means that nearly all mortgages originated by Figure or its partners through the LOS are subsequently sold to investors on the Connect marketplace.

With LOS, Connect, Democratized Prime, securitization capabilities, and in-house servicing, Figure vertically integrates the entire non-QM process. Figure started in HELOCs but recently expanded to DSCR loans and crypto-backed loans. Furthermore, its HELOC product is tapping into more than just subordinate loans, with 20% of its volume being first-lien as of Q3.

Source: Figure’s Q3 earnings presentation

The Big Unlock: Figure Certified

Mortgages originated through Figure’s processes will continue to power Connect ’s growth, but the next major catalyst will come from introducing Figure Certified. While details remain limited, Figure’s November 2025 S-1 provided some additional context:

We are introducing a Figure Certified program that employs proprietary technology and artificial intelligence to validate assets originated by third parties outside of our platform against our LOS underwriting guidelines, such that we can confidently tokenize the loans on the Provenance Blockchain and also support the sale of those assets via Figure Connect. Figure Certified loans would be allowed to transact in Figure Connect, increasing the scope of our marketplace beyond our LOS originated assets without losing the benefits of homogeneous collateral. We are targeting a launch of the Figure Certified program by the fourth quarter of 2025.

Figure was targeting a Q4 launch, but it does not appear to have launched as of today. Once operational, Figure Certified will expand the company’s addressable market to all non-QMs and other types of credit (auto and personal loans). This will allow it to address the entirety of the ~$90 billion non-QM market and create a Connect marketplace that can facilitate multiples of that in transactional volume per year. Eventually, if Figure creates enough of a standardized process, we could see it start to capture some of the QM volume from their origination partners who already leverage Figure for HELOCs. This addressable QM origination volume is in the hundreds of billions per year just from Figure’s existing customer base.

Figure has built the infrastructure to do for non-QM what Fannie and Freddie did for conforming mortgages, and it now offers the end-to-end solution to create a liquid, standardized marketplace that could increase efficiency and expand the overall market. A future post will go into the mid-term investment thesis in more detail, including how I’m modeling growth and different scenarios.

[1] Figure public filings, MBA

[2] As of February 4, 2026, per DefiLlama

[3] Bloomberg

[4] JPMorgan

[5] Freddie Mac, MBA

[6] MBA, HMDA

[7] MBA

[8] Fannie Mae

[9] MBA’s 2025 IMB Fact Sheet

[10] SIFMA

[11] MBA

[12] Bernstein

[13] Freddie Mac