Fintech on File #5 | Kraken IPO back on; Big Banks show resilient consumer; Airwallex hits $300B scale; AmEx goes agentic

April 20, 2026

Deal Room

Kraken IPO Plans Thaw After Winter Freeze

Kraken co-CEO Arjun Sethi confirmed at the Semafor World Economy Summit on April 14 that the exchange’s confidential S-1 — first filed in November 2025 — remains active, walking back March reports that the IPO had been shelved amid the crypto selloff. The clarification came the same day Deutsche Börse took a ~$200M secondary position (~1.5% fully diluted) at a $13.3B valuation, a 33% haircut from the $20B November round that included Citadel Securities and Jane Street. With the S&P 500 back at all-time highs, BTC at $75K, and CLARITY moving along, we may see Kraken test the markets sooner rather than later.

The Print

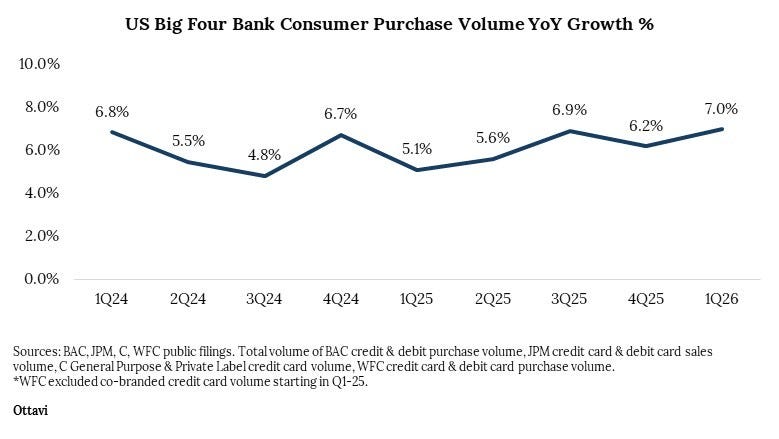

Q1 earnings from the Big Four money center banks landed last week, offering an updated read on consumer spend. Total payment volume growth across JPMorgan, Citigroup, Wells Fargo, and Bank of America was up 7% year-over-year — accelerating 80 basis points from Q4. Consumer spending remains resilient. We’ll get another look at the US consumer when Visa reports on April 28.

Fintech In The News

Once close enough for an acquisition, Stripe and Airwallex are now going after each other | TechCrunch

TechCrunch reported Airwallex — dual-headquartered in Singapore and San Francisco headquartered — generated $300B in annualized payment volume and $1.3B in annualized revenue, growing 85% year-over-year. $300B in volume puts Airwallex at a similar scale to Checkout.com, which reported $300B in total volume in 2025. At ~43 basis points, Airwallex’s revenue should be a relatively close proxy for net revenue and gross profit, given this is roughly on par with Stripe’s blended take rate which is net of interchange and other pass-through costs.

Airwallex is building the global cross-border SWIFT alternative by going the hard route of building its own infrastructure, including obtaining 90 licenses with regulators and central banks across the 50 markets it currently operates in. Airwallex is taking a similar path similar to Adyen, which is notorious for building the cornerstone of its advantages through a single tech stack and directly connecting to central banks. It takes longer to scale but confers more control and advantages – allowing faster scale once the pieces are in place.

The slow build was intentional, and Zhang has a framework for it that he returns to often: the “path of maximum resistance.” Every license, every bank integration, every local payment rail that Airwallex painstakingly assembled has created a layer that makes it harder to compete against. “It took us six and a half years to get to $100 million in annual recurring revenue,” Zhang said. “But after that, it took just over three years to get to a billion.”

American Express Debuts Agentic Commerce Experiences (ACE)™ Developer Kit and Announces Industry-First Protection for Registered Agent Purchases | American Express

American Express rolled out its ACE developer kit on April 14 — a framework of five integrated services (Agent Registration, Account Enablement, Intent Intelligence, Payment Credentials, Cart Context) designed to route AI agent transactions through Amex rails with authenticated intent. The headline commitment is Amex Agent Purchase Protection: if a registered agent completes a purchase based on authenticated intent and gets it wrong, Amex covers the eligible charge.

American Express is leveraging its closed-loop network advantages, and this marks the first meaningful step toward an issuer-backed guarantee for agentic commerce. I expect issuers reliant on the Visa and Mastercard four-party model to adopt a similar guarantee – or at least, this should accelerate the discussion around agentic commerce liability.

Regulatory Radar

Treasury/IRS Propose Rules for 1% Outbound Remittance Excise Tax Under “One, Big, Beautiful Bill” Act | Link

The proposed regulations clarify that the tax applies to cash, money orders, and similar physical instruments — with bank account and U.S. debit/credit card-funded transfers explicitly excluded. That carve-out is the key tell: cross-border flows routed through fintechs using stablecoins or card rails effectively avoid the tax, while legacy cash-based remitters (WU, MGI, and the informal market) absorb the friction. Comments are due June 12. For fintech cross-border names, this is a meaningful tailwind disguised as a consumer tax.

Data That Matters

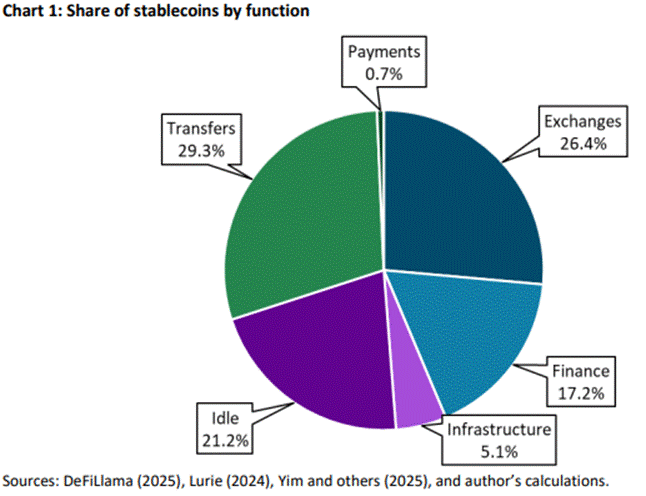

Kansas City Federal Reserve’s Franklin Noll Estimates Payments at 0.7% of Total Stablecoin Volume | Link

Kansas City Federal Reserve’s Franklin Noll published a report estimating the share of stablecoin volume by function. Much of stablecoin volume is used for trading-related activity and settlement, with only 0.7% of volume related to payments. Noll drew on analysis from Visa, which tracks stablecoin volume — including retail payments — through its Onchain Analytics Dashboard. For all the fervor, stablecoins use for payments remains nascent.

Noll’s three takeaways:

First, payments are still a very small part of the world of stablecoins, accounting for less than 1 percent of all stablecoin use. Here, payments defined in the traditional sense of B2B, P2P, and so on, have yet to live up to the promise of explosive growth proclaimed by many since the passage of the GENIUS act in July 2025. However, the use of stablecoins in payments is undoubtedly growing.

Second, more than 5 percent of stablecoins are tied up in the infrastructure of the stablecoin ecosystem, primarily bridges, indicating that interoperability problems exist. In fact, given the many infrastructure services provided by exchanges, the portion of stablecoins devoted to the machinery required to move tokens across chains and facilitate stablecoin usage may be understated.

Third, although stablecoins are widely believed to have the potential to operate independently of crypto finance, nearly half of all stablecoins continue to be used in crypto finance, including exchanges, finance, and infrastructure protocols, with CEXs and DEXs playing major roles. Overall, the large role played by crypto finance in the stablecoin ecosystem also suggests that the entire ecosystem is sensitive to the vagaries of crypto finance, rising and falling with the market.

This Week’s Media

“Beyond the Sky” by Colossus

Dom Cooke’s Colossus profile of Hyperliquid and founder Jeffrey Yan — the product of a week embedded at Hyperliquid’s Singapore office — is the definitive piece on what may be the most consequential under-the-radar story in financial services right now. Eleven employees generated over $900M in profit last year at a $10B market cap, with zero VC funding and roughly 37% share of decentralized perpetuals — all while Americans are locked out of Hyperliquid under Dodd-Frank, which requires every derivatives transaction to flow through a regulated intermediary. Yan’s ultimate goal is to be the “house of finance” while maintaining decentralization. Yan turned down a ~$100M offer at a $1B valuation on principle, arguing the protocol needs to remain neutral. Whatever your view on Hyperliquid, this is well worth the read on a company making serious inroads in financial services.

The Week Ahead

Earnings are in full swing after big banks reported last week. Notable fintech earnings coming up this week are as follows:

• Monday, April 20: None

• Tuesday, April 21: Interactive Brokers (IBKR)

• Wednesday, April 22: None

• Thursday, April 23: Nasdaq (NDAQ), AppFolio (APPF)

• Friday, April 24: None