Fintech on File #2 | Stablecoins et al

March 15, 2026

This week’s edition has a heavy stablecoin focus. This was unintended, but a sign of the current times I suppose.

This Week’s Reads

Stablecoins Are Not Free — Why They Are A RAIL in Consumer Payments | Starpoint by Tom Noyes

Tom Noyes’ blog Starpoint is recommended reading for anyone trying to learn the nuts and bolts of payments. His post today on stablecoins is no exception. Noyes’ view aligns closely with my own on the stablecoin debate. For consumer payments, stablecoins are likely to become another rail and used as plumbing, with the existing four-party model remaining intact with Visa and Mastercard retaining their position as the orchestration layer. Stablecoin adoption as a payment instrument seems more likely to gain traction in other segments — agent-to-agent (A2A), business-to-business (B2B), micropayments, and cross-border. Payments are not a monolith, even if the sector is commonly framed by investors through the consumer-to-business lens. None of this is to say stablecoins won’t see massive adoption — just not in the manner many assume.

“There’s a narrative running through payments circles right now that goes something like this: stablecoins will replace card rails because they’re cheaper, faster, and programmable. Stripe makes acceptance easy. Card networks are too slow to innovate. Machine-Machine payments need programmability. GENIUS Act passed. The future is obvious...I keep coming back to the same conclusion: stablecoins are not a replacement for cards, but rather another rail with cards retaining their role as the layer of abstraction for multiple networks (as they do today). They will do well where cards don’t play (micropayments, B2B and uncarded markets).”

Fintech In The News

Mastercard launches new Crypto Partner Program | Mastercard

Mastercard has launched a formal Crypto Partner Program — a global initiative bringing together more than 85 crypto-native companies, payments providers, and financial institutions to co-develop the next generation of onchain payment products. The program reflects a core belief that the next phase of onchain payments will be built through collaboration. Participants will engage with Mastercard teams on the design and direction of future products and services, including solutions that aim to combine the speed and programmability of digital assets with established card rails and global commerce flows. The partner ecosystem spans every layer of a crypto payment stack — blockchain rails including Solana, Polygon, and Cosmos, and custody infrastructure from Fireblocks, BitGo, and Anchorage Digital. Mastercard’s objective is to embed itself as the authentication, governance, and settlement layer for the onchain commerce era.

Ramp Launches Agent Cards | Ramp

Ramp officially launched its Agent Cards feature on March 11, designed specifically for AI agents that need to make purchases on behalf of users or businesses. The feature gives agents the ability to spend — governed by real spend limits, merchant controls, and full visibility into every transaction — without exposing sensitive card information. At the core of the system is a per-transaction tokenized credential architecture powered by Visa’s Intelligent Commerce protocol and Trusted Agent Protocol, ensuring each credential is temporary and transaction-specific; credentials can be generated via API, MCP, or CLI, making it adaptable for developers at any scale.

Stanley Druckenmiller: “I assume our whole payment systems will be stablecoins in 10 or 15 years.”

In a Morgan Stanley interview released March 13, Duquesne Capital founder Stanley Druckenmiller said blockchain and stablecoins are “incredibly useful in terms of productivity” and “assumes” the entire global payment system will run on stablecoins within 10 to 15 years, calling them more efficient, quicker, and cheaper than existing infrastructure. Druckenmiller critiqued broader crypto as “a solution looking for a problem” — drawing a sharp line between stablecoins and blockchain as infrastructure and crypto as a store-of-value asset.

Data That Matters

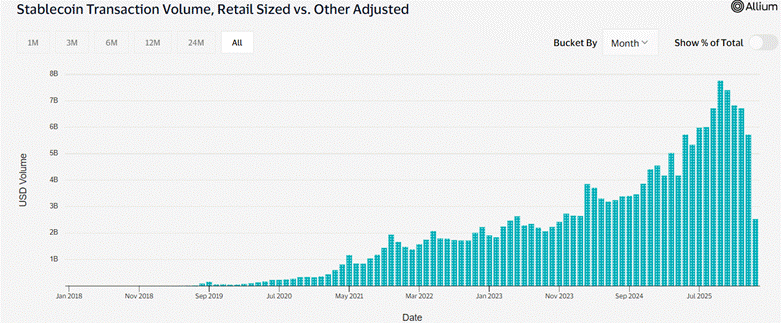

Given the topic du jour, I thought it would be valuable to reference data on where the stablecoin industry currently sits. Visa’s Onchain Analytics Dashboard created in partnership with Allium, estimates adjusted stablecoin volume to arrive at a more like-for-like transaction volume figure reported by Visa, Mastercard, and other payments companies. Visa estimates that ‘retail-sized’ transaction volume — its proxy for consumer-based payment volume — was $5.2B monthly, or $62.4B annualized. That represents roughly 0.3% of Visa and Mastercard’s combined payment volume of more than $23T in 2025. McKinsey, in partnership with Artemis Analytics, also published a helpful report on this topic.

Source: Visa Onchain Analytics Dashboard

*From Visa’s Onchain Dashboard: Visa adjusts stablecoin transaction volume. Only categories including centralized exchanges, decentralized exchanges, Lending, Mint/Burn, etc. and addresses, and their associated transactions, are included if the address has not sent more than 1,000 transactions or $10m in transfer volume in a given 30-day period. This removes high-frequency and high-volume trading wallets, high-frequency and high-volume smart contract addresses, bot related activity. Retail Sized are transactions that fall under any of the Adjusted Categories and that are also less than $250.

Deal Room

PayPay IPO Follow-up

Quick follow-up on the PayPay IPO covered in the March 11 edition. PayPay’s stock finished at $18.16 on March 12, up 14% from the $16 IPO pricing. The stock closed Friday at $21.14, up 32% in its first two trading days. Solid investor demand for PayPay in what was a volatile week given the Iran conflict.

Admittedly, I don’t ‘get’ stablecoins. Yes, they’re cheaper b/c their advocates choose to drive adoption, not turn a significant profit. Visa and Mastercard could too offer cheap transaction processing if they abandoned their profit motive, but they’ve already gained global ubiquity and orchestrated a beautiful experience for consumers. Once stablecoins are able to do that, I’m guessing they too will want to turn a nice profit.