MercadoLibre, Shopee, and the Battle for Brazil

MELI & SE Underperformance

Stock returns for MELI and SE have lagged the broader tech indices materially since MELI cut its free shipping threshold in early June from R$79 (~$15) to R$19 (<$4). MELI’s underperformed by 37%, while SE has lagged by 35%. The graph below shows SE’s and MELI’s absolute performance and relative performance to QQQ.

Source: Bloomberg

The divergence between the market was more pronounced initially for MELI and has persisted through November, while SE’s underperformance occurred more recently, following revisions to Shopee’s margin estimates. MELI’s reaction was a direct response to SE’s competitive threat in Brazil, while SE’s more recent selloff is partially due to a more competitive Brazil and to investments SE is making in its core Southeast Asia markets.

MELI and SE’s recent stock underperformance has sparked a debate on X. While most likely aren’t looking for another opinion on the topic, I wanted to add a more nuanced perspective. A few thoughts:

MELI remains the scaled #1 player in Brazil across ecommerce and financial services. I suspect this will remain true for the foreseeable future.

SE’s Shopee has done an admirable job of scaling in an area of the market that MELI ignored (lower-income consumers, low average order values). It has used its strategy to scale a business that’s #2 to MELI in GMV and revenue, and #1 in metrics, like total active users and orders. SE’s built enough of a business with this focus that it is here to stay long-term and is now trying to move up-market into MELI’s core business.

SE’s momentum and scale were sufficient for MELI to fight back, including impairing its unit economics by lowering its free shipping threshold materially.

#3 being true does not mean #1 or #2 cannot also be true. Brazilian ecommerce is consolidating into a duopoly, and MELI and SE are both growing profitably. The market still remains under-penetrated with estimates of only a mid-teens percentage of the market conducted online. There will be room for both MELI and SE to grow in the foreseeable future. However, there are legitimate questions about MELI BZ’s profit margins going forward if SE continues to gain overall market share.

Signal vs. Noise: Direction of the Fundamentals

It can be tempting to look at a stock’s underperformance and state that the market is being irrational. However, a stock’s performance needs to be put into the context of how new information has impacted the market’s expectations for future free cash flow generation. Since May, consensus estimates for MELI Brazil’s 2026 contribution profit are down by 34% due to the reduced free shipping thresholds and investments in sales and marketing to drive stronger top-line growth.

Source: Bloomberg

In 2024, Brazil accounted for 46% of MELI’s total contribution profit (before accounting for corporate costs and other overhead). Unsurprisingly, as MELI BZ’s profit estimates got cut, so too did overall estimates. MELI’s 2026/2027 consensus adjusted EPS estimates peaked in early June and have been in a downward trajectory since, coinciding with the free shipping reduction. Since then, MELI’s 2026/2027 adjusted EPS consensus estimates are down ~13% and ~10%, respectively (the graph below overlays MELI’s stock price with changes to 2026/2027 adjusted EPS estimates). Importantly, this is the first time since SE entered the Brazilian market in 2019 that forward-looking estimates have been revised downward due to SE’s risks. When put into this context, it’s unsurprising that MELI’s stock has underperformed over the last several months.

Source: Bloomberg

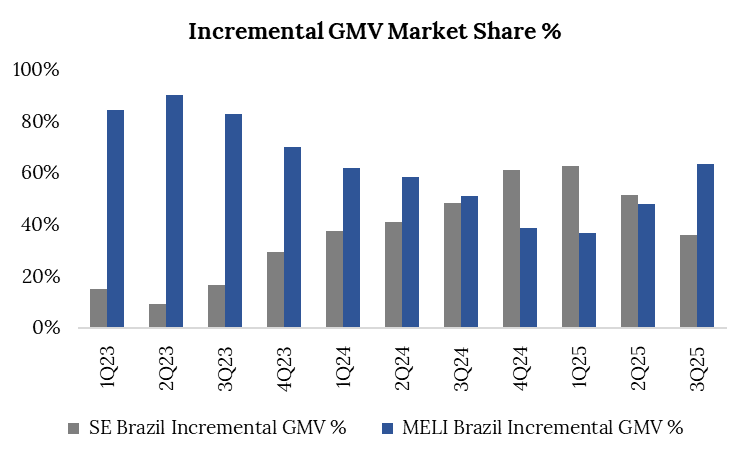

The incremental growth shows why MELI is taking margins down. From 3Q24-2Q25, Shopee’s incremental growth was approximately at par or above MELI’s. While MELI’s overall market share is materially larger than Shopee’s (estimated at ~2x), the incremental growth painted a potentially weaker outlook. However, 3Q25’s incremental growth reverted in MELI’s favor for the first time in 5 quarters, showing that the actions are helping MELI grow incremental share again.

Sources: MELI and SE public filings, Ottavi.

*Note: GMV is calculated in USD. Shopee Brazil’s GMV are Ottavi estimates given it is not reported by SE.

Additionally, SE’s credit expansion (through its Monee unit) likely raised more concerns at MELI, prompting it to act now. In emerging markets like Brazil, ecommerce and financial services are synergistic. Many Brazilians pay for ecommerce purchases with short-term loans due to lower disposable income and high inflation rates. On the back of securing a Sociedade de Crédito Direto (SCD) license in August 2025, which allows it to lend with the company’s own funds, Monee’s loan growth was 3x year-over-year in 3Q25, after growing 2x year-over-year in 2Q25. It’s still a small fraction of MELI BZ’s loan book, but is incrementally scaling quickly.

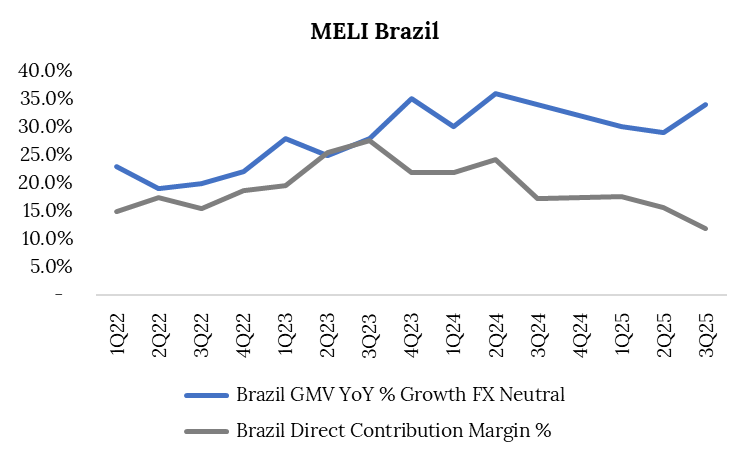

Perhaps the most telling graphic is the ~2-year downward trend for MELI BZ’s contribution margins after peaking at 28% in 3Q23. In 3Q25, MELI Brazil’s margins contracted further to 12%, down more than 370bps quarter-over-quarter, 550bps year-over-year, and nearly 1,600bps since the 3Q23 peak. There are multiple factors at play but it seems clear that MELI is responding to the growing threat from Shopee.

Sources: MELI public filings, Ottavi.

Closing Remarks

Are 3Q25 margins the floor and do contribution margins stabilize from here? Will SE successfully move up-market and put additional pressures on MELI’s margins? Will MELI’s actions use the might of the scale it’s built and force SE to choose between growth and profitability? Or do MELI and SE grow rationally with both generating profitable growth with margin expansion? Ultimately, MELI’s stock performance over the next 1-2 years will at least partially depend on answers to these questions and how they impact the direction of the lines above.