Payments: Assessing the AI, Agentic, and Stablecoin Risks for Merchant Acquirers

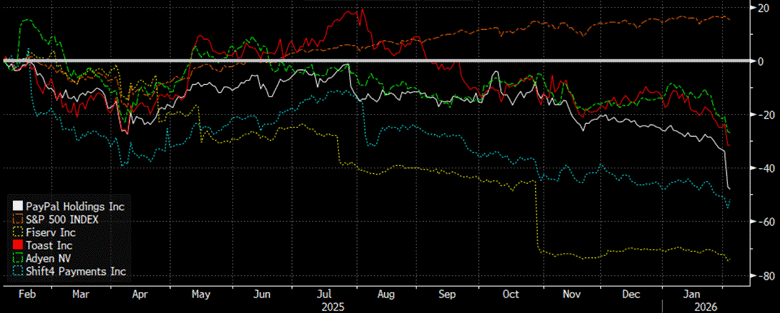

In the midst of the AI-driven software selloff, payments stocks were also hit hard. PayPal’s (PYPL) bad earnings didn’t help matters. This led $PYPL to reset expectations again with CEO Alex Chriss terminated after running the company since September 2023. PYPL’s stock finished down ~20% on the day, while other payments companies were also down double digits. This follows the $FISV -40%+blowup in October after the company announced a materially lower organic growth outlook (among other idiosyncratic factors). This caused further flows out of publicly traded merchant acquirers.

In total, all public merchant acquirers are down over the past year, with relative underperformance versus the S&P 500 ranging from 42% ($ADYEN.NA) to 89% ($FISV).

Source: Bloomberg

An increasing number of companies trade for single-digit P/E multiples, which implies the market believes these companies are facing terminal risks and will not be able to sustain even modest levels of EPS and FCF per share growth. This post focuses on the existential risks (AI, agentic, stablecoins) rather than any specific individual stock.

Quick Payments Primer

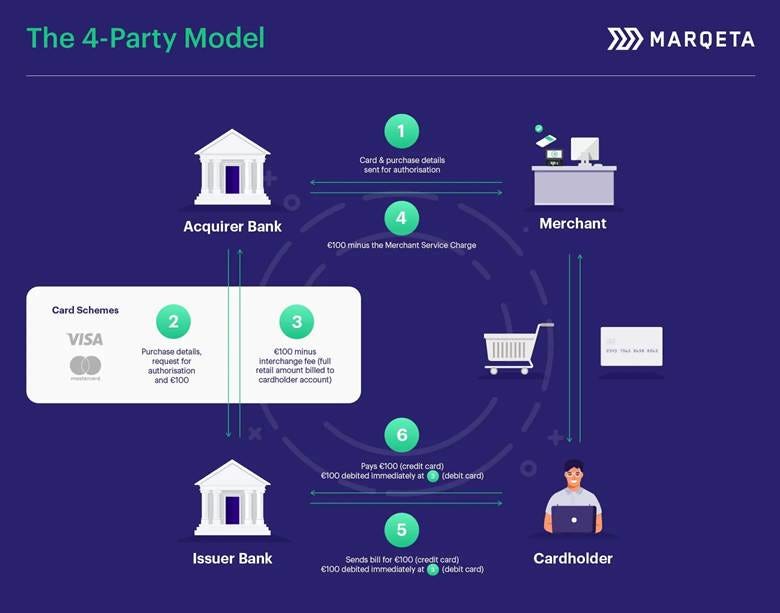

As a quick primer, most US-based digital payments are transacted through the four-party model popularized by Visa ($V) and Mastercard ($MA). These networks sit at the middle of the ecosystem as the orchestration layer, setting rules and facilitating communication between merchant acquirers and card issuers. American Express ($AXP) and Discover (now part of Capital One, $COF) operate closed-loop models where they control all major aspects of the payment process. This write-up focuses on the merchant acquirers (“banks” in the graphic below), which include Adyen ($ADYEN.NA), Block ($XYZ), Fiserv ($FISV), Global Payments ($GPN), PAR Technology ($PAR), Shift4 ($FOUR), Stripe (private), and Toast ($TOST).

Source: Marqeta

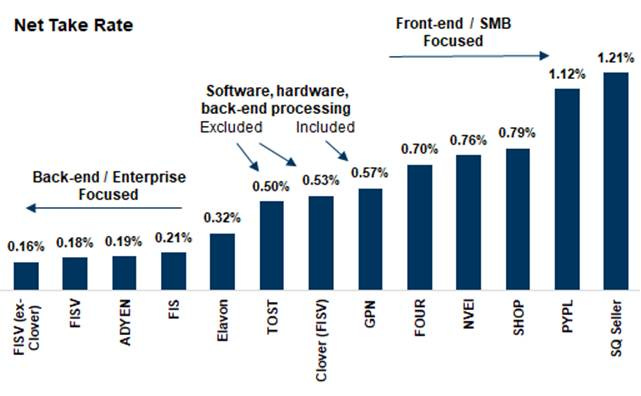

Acquirers contract directly with merchants, simplifying the process for them to accept payments. Acquirers handle funds flow, fraud detection, and chargebacks. In exchange, acquirers capture a net take rate of approximately 10–120 basis points. The graphic below is from Goldman Sachs; it is somewhat dated (2022), but the figures have not changed substantially, and the general premise still holds: the take rate spectrum increases as you move from enterprise clients to SMBs. Similarly, the more of the payments stack a processor controls in-house, the more economics it captures.

For example, Toast ($TOST) operates as a payments facilitator (PayFac), meaning it handles the front-end but partners with an acquirer (such as Worldpay or Adyen) and therefore gives away some of its economics. By contrast, Shift4 ($FOUR) handles acquiring in-house and captures more of the payments economics than Toast, even in a common vertical like restaurants.

Source: Goldman Sachs

Source: Goldman Sachs

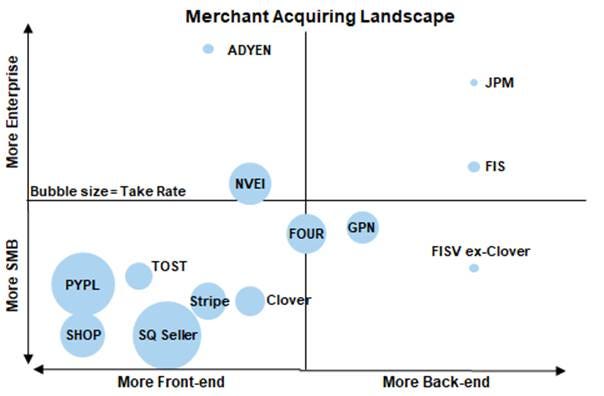

While all the businesses listed above operate in the payments space, there are nuances in their models. Some subsidize hardware costs ($FOUR), while others generate a meaningful portion of their revenue from software ($TOST, $SHOP). Some focus on organic growth, while others pursue an acquisitive strategy.

Historically, merchant acquiring has been a competitive business and the industry continually moves toward commoditization. Even with these challenges, merchant acquirers have shown to have retentive merchant bases, stable take rates (on a like-for-like basis), and generate significant free cash flow. However, the payments landscape is experiencing more potential change over the coming years than it has in maybe the last few decades. There are three fundamental potential changes happening to the ecosystem: AI-Driven Innovation, agentic commerce, and stablecoins.

AI-Driven Innovation

If AI significantly reduces the cost of software development, this could theoretically create an increasingly competitive playing field (in a market that is already crowded). However, building a payments company is more challenging than “vibe-coding” a competitor. Creating a viable payments operation requires the ability to facilitate money movement. Even if a startup takes the PayFac route (partnering with an acquirer), it still must register with different payment networks, partner with an acquiring bank that underwrites payment risks, and meet extensive compliance requirements (e.g., PCI DSS Level 1 Certification, state money transmitter licenses, KYC, AML). While not impossible, these requirements demand significant capital and resources, creating meaningful barriers to getting started. Some acquirers, like Adyen ($ADYEN.NA), hold banking licenses and are integrated directly with central banks, providing additional competitive advantages.

Furthermore, in physical retail, cloud-based acquirers have taken significant share from legacy providers (NCR, MICROS), but they have achieved this through distribution networks. Selling physical hardware to SMBs requires “feet on the street.” In payments, distribution has proven to be a relatively defensible strategy. Legacy merchant acquirers still retain something like half of the US restaurant market even with the success of $TOST, $XYZ, $FOUR, and $PAR. Even if a vibe-coded competitor integrated payments, it would likely need to build out a salesforce to execute on its strategy.

Alternatively, AI may provide a net benefit to acquirers through improved fraud detection. Adyen Uplift—Adyen’s AI module—leverages over $1 trillion in annual payment volume to reduce fraud and increase conversion rates. In select case studies, $ADYEN has found authorization rates increase by 6% with Uplift. While fraud is not as significant a concern in physical retail, it remains prevalent in e-commerce. Although Adyen Uplift is still in early stages, this capability is expected to be a tailwind to monetization and should allow Adyen to capture greater wallet share versus subscale processors.

One risk to existing acquirers would be if those who have historically charged premiums for software revenues experience deflation—or impaired pricing power—because competitors that have historically had weaker R&D innovation see the playing field leveled by AI-generated code (consider $FOUR versus $TOST).

Agentic Commerce

It seems inevitable that AI agents will make purchases on behalf of consumers in the not-too-distant future. Unless robots advance to the point of physically purchasing goods for us, this is primarily a consideration for e-commerce acquirers.

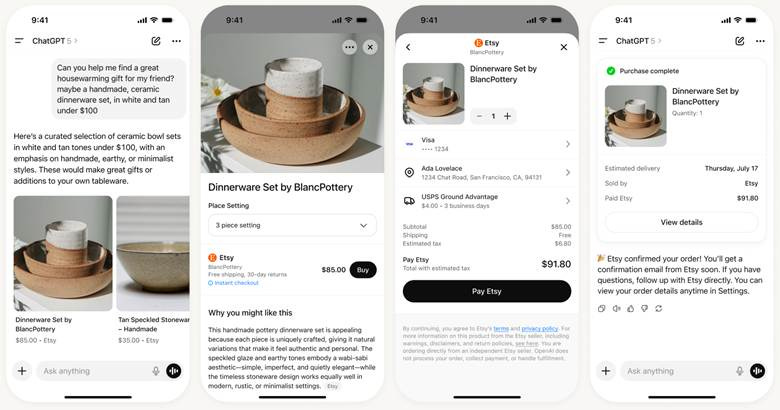

Agentic commerce would present potential risk if it disintermediated acquirers from the checkout process. However, this scenario seems unlikely. Current evidence suggests that agentic commerce will leverage existing payment rails rather than circumvent the current system. For example, ChatGPT Instant Checkout—which allows consumers to purchase products within the ChatGPT experience—requires consumers to click a “buy” button to confirm payment details and complete the purchase, following the standard e-commerce checkout process. Currently, ChatGPT Instant Checkout is powered by Stripe and Shopify (which itself uses Stripe), with payment fees comparable to traditional e-commerce purchases (2.9% + $0.30). This excludes the fee ChatGPT charges in addition to this for demand generation.

ChatGPT Instant Checkout experience

Source: ChatGPT

One counterargument is that the current experience is human-led and feels analogous to purchasing in any other e-commerce marketplace, rather than a truly autonomous agent completing the purchase for the consumer—which is where the market will inevitably evolve to. That is valid, but it still seems more likely than not that agents will leverage existing infrastructure rather than build entirely new payment rails. One could argue that the proliferation of agents will actually require more safeguards around payment identification, which is precisely where existing payments infrastructure is well-positioned. For example, $V launched Visa Intelligent Commerce in April 2025, which works to identify agents and provide them with tokenized credentials to reduce fraud and facilitate seamless future purchases. If agentic commerce rides the $V / $MA rails then acquirers should remain well-positioned as the four-party model remains intact.

However, agentic commerce does open the possibility for new types of consumption that do not currently exist at scale. Consider micro-transactions: in-app purchases or access to individual articles behind hard paywalls. If micro-transactions end up being significantly smaller than the average purchase today (e.g., $0.50 for an article), the economics of the existing payments model do not work. Using Stripe’s 2.9% + $0.30 pricing, $0.31 of the $0.50—or 62% of the transaction value—would go to Stripe, leaving little for the merchant. While the 2.9% + $0.30 rate is for SMBs, even interchange++ pricing (common for enterprise merchants) would still consume much of the transaction value given there is typically a fixed cost component that goes to the acquirers. Ultimately, the pricing model would need to change. Either transactions would need to be batched, or models would need to evolve. This could open bottom-up disruption from stablecoins, which offer an orthogonal approach to disrupting payments given traditional acquirers likely cannot address these volumes through their existing economics.

Stablecoins

Stablecoins have scaled rapidly in recent years, bolstered by the passage of the GENIUS Act in July 2025. Stablecoins promise cheaper, faster, programmable money that has the potential to disrupt global payments. According to Artemis Analytics, stablecoin transaction volume is at an approximately $35 trillion run-rate. However, much of this volume currently facilitates or settles exchange trading volumes rather than payments for products or services. Retail-based stablecoin payments are still nascent compared to Visa and Mastercard’s combined global payments volume, at ~$76 billion, which is 0.3% of Visa and Mastercard’s combined global payments volume of $23+ trillion in 2025. It seems that stablecoins are most likely to address cross-border, business-to-business, and treasury money movement rather than consumer-based-payments (in the US).

Even in a scenario where stablecoin payments take meaningful share from traditional card-based payments, volume shifts would likely be gradual rather than abrupt. In such a scenario, merchants will not want multiple acquirers. This is particularly true for physical commerce merchants that tend to route 100% of their volume through one acquirer, which is integrated with (or even provides) their payment checkout hardware.

It seems more likely that stablecoins become another payment rail that acquirers accept on merchants’ behalf. The increasing complexity is actually a net benefit to acquirers who can simplify the process for merchants to accept multiple payment methods (cards, BNPL, account-to-account, Venmo, stablecoins). An increasing number of merchant acquirers already provide the ability to pay with stablecoins at checkout.

Stablecoins could also benefit merchants through faster settlement. Shift4 ($FOUR) announced in December 2025 that it is allowing merchants to settle with stablecoins instead of bank transfers, enabling 24/7 fund movement.

This was a quick overview of how I view AI, agentic, and stablecoins but is by no means an exhaustive analysis of each. Some of these areas are quickly evolving so my opinion may change as the facts do. Any thoughts or pushback is welcomed.