Stripe vs. Adyen Comparison (2025)

Stripe published its 2025 annual letter this morning. Some takeaways when comparing to Adyen:

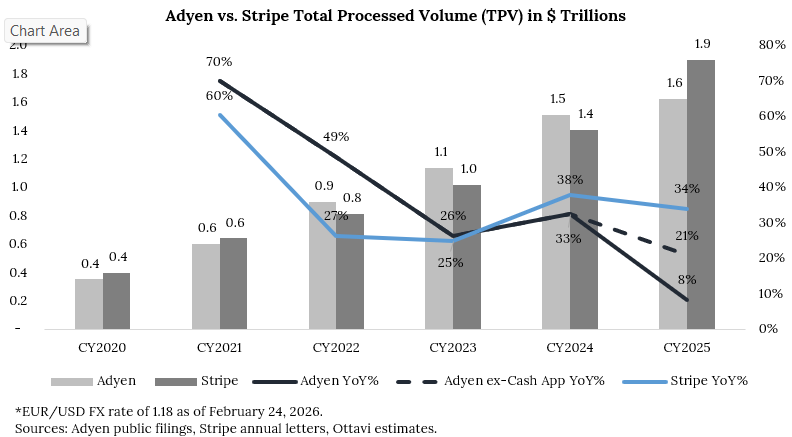

Comparing to Adyen, Stripe grew volumes materially in 2025 (34% YoY) no matter how you look at Adyen’s volume - reported volume growth was 8% YoY or 21% when adjusting for the loss of Cash App business.

2025 was the first year Stripe surpassed Adyen’s volume at ~$1.9T vs. Adyen at ~$1.6T. I converted Adyen’s volume to USD to make it more comparable.

Total processed volume only tells part of the story though considering enterprise volume for Stripe is I believe ~50-60% of their total volume with the remainder SMB. Adyen is essentially all enterprise - meaning their enterprise volume is still likely ~40% larger than Stripe (but these are just my estimates not reported figures).

Both Adyen and Stripe stated the 2025 cohorts were their largest ever. Stripe benefiting disproportionately from new AI company formation: “In 2025, many more new companies joined Stripe than ever before, with more than half of them (57%) based outside the US. This new cohort is by far the highest performing and fastest moving we’ve ever seen, growing around 50% faster than the 2024 cohort. The number of companies reaching $10 million ARR within 3 months of launch was double the 2024 count.”

Net take rates are meaningfully different for Adyen and Stripe. Enterprise net take rates are similar for both (~16-20bps) but Stripe’s blended take rate is likely ~2x higher given their SMB mix (SMB net take rates are likely above 50bps+) putting consolidated take rates at ~35bps for Stripe. Additionally, non-payment revenue is becoming more meaningful for Stripe - the letter cited a target of $1B+ annual run-rate in 2026. Non-payment revenue is likely LDD% of total revenue for Stripe (ADYEN gives little disclosure here).

In total, net revenue for Stripe at ~$6.8B versus Adyen at ~$2.8B. Adyen likely has higher EBITDA margins than Stripe (53% in 2025 vs. unknown for Stripe) but a significantly smaller revenue base.

Stripe tendered shares at $159B this month, up 74% from the ~$91.5B Stripe tendered shares at in February 2025. This compares to Adyen’s current market cap at ~$35B (down ~47% over the past year). Stripe’s 350%+ valuation premium vs Adyen is widest it’s ever been.

One could argue Stripe would be valued higher than Adyen if it were public today (growing faster, more tangible AI benefits to growth) but the gap feels too wide to me. Adyen is expected to grow EBITDA ~20% YoY in 2026 and trades for 12.7x 2026 EBITDA. Let’s assume Stripe grows revenue at ~30% in 2026 and put the EBITDA margin range at 30-50% (wide range I know) - this puts Stripe’s 2026 EBITDA at $2.7-4.4B* or a multiple at 36-59x.**

*This accounts for SBC to try to make like-for-like with Adyen.

**Cash is not reported by Stripe but the company is likely in a net cash position, meaning the actual multiple would be lower than this range. This is meant to be directional.