The (Ecommerce) Agents Are Coming

With the onslaught of agentic commerce announcements — Google’s UCP, OpenAI’s ACP — the debate about what commerce looks like in an agentic world is intensifying. As LLMs improve and agents become more capable, it’s unlikely to quiet down.

I previously wrote brief thoughts on agentic commerce (which was more from a payments perspective), concluding that “it seems inevitable that AI agents will make purchases on behalf of consumers in the not-too-distant future.” I wish I’d phrased that differently. While agents completing much of the purchase journey end-to-end is plausible in the near term, the reality will be far more nuanced — both by category and by the specific criteria that define each shopping experience.

How agentic commerce evolves will depend on advancements in LLMs, which parts of the value chain agents control, and how both shape consumer behavior. What I’m confident in is this: agentic commerce is unlikely to evolve in one monolithic way — just as ecommerce hasn’t, and in-person retail before it. The nuance will live in the category. Agentic commerce for groceries will look fundamentally different from booking a hotel or buying clothing. Even within a single platform, categories are treated very differently — consider Amazon’s grocery strategy versus its apparel vertical.

The Current State

In September 2025, OpenAI announced its Agent Commerce Protocol (ACP); Google followed with its Universal Commerce Protocol (UCP) in January. Both attempt to solve the coordination complexity inherent in multi-party commerce. Without universally accepted protocols, every player would need bespoke agreements with each other — an NxN problem that would make agentic commerce dead on arrival. ACP and UCP try to solve this by creating unified standards for all parties to follow.

Neither protocol is guaranteed to succeed. Notably, Amazon is holding out, prioritizing its closed ecosystem and protecting its first-party data and advertising business. The walled-garden versus open-protocol tension we see across the internet today may well persist in an agentic world. But given the scale of both Google and OpenAI, these protocols seem likely to anchor significant portions of how agentic commerce develops.

In both ACP and UCP, the merchant remains the merchant of record — responsible for everything that happens after the consumer initiates a purchase. The architectures differ meaningfully, though. ACP is structured with ChatGPT as the front-end aggregator owning discovery, with OpenAI taking a ~4% transaction fee for that aggregation role.1 Google’s UCP is more open-source in nature, providing a fuller framework across the commerce journey — including post-purchase elements like returns, an area where ACP offers comparatively little guidance.

The current iteration of both shopping experiences feels less like agentic commerce and more like search-led commerce with conversational LLM-based discovery replacing keyword search. The checkout experience remains largely unchanged, payments infrastructure is identical to traditional ecommerce, and the merchant retains responsibility for logistics and post-purchase operations — as the Etsy and Wayfair examples illustrate.

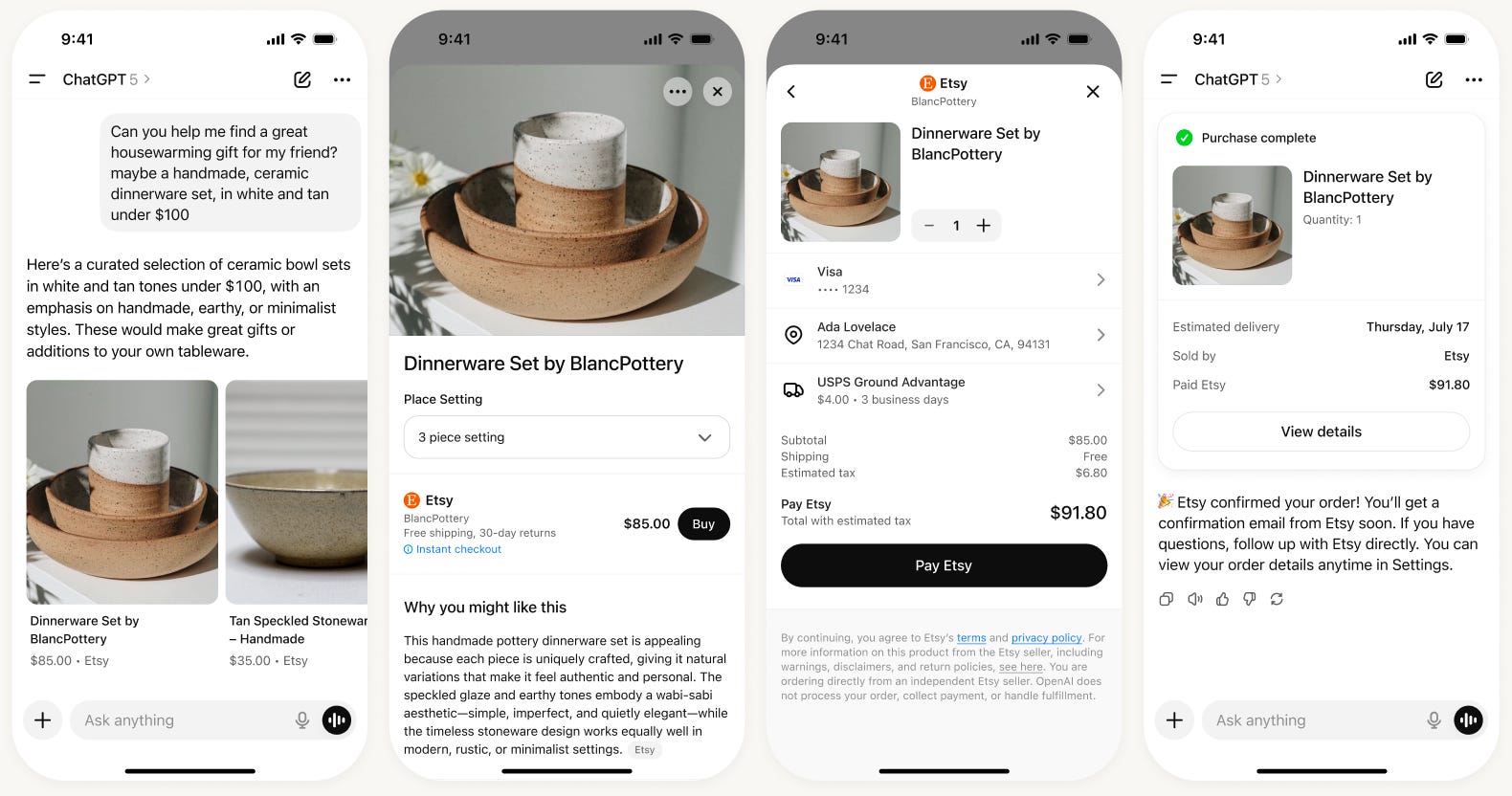

OpenAI’s ChatGPT Instant Checkout Experience with Etsy

Source: OpenAI

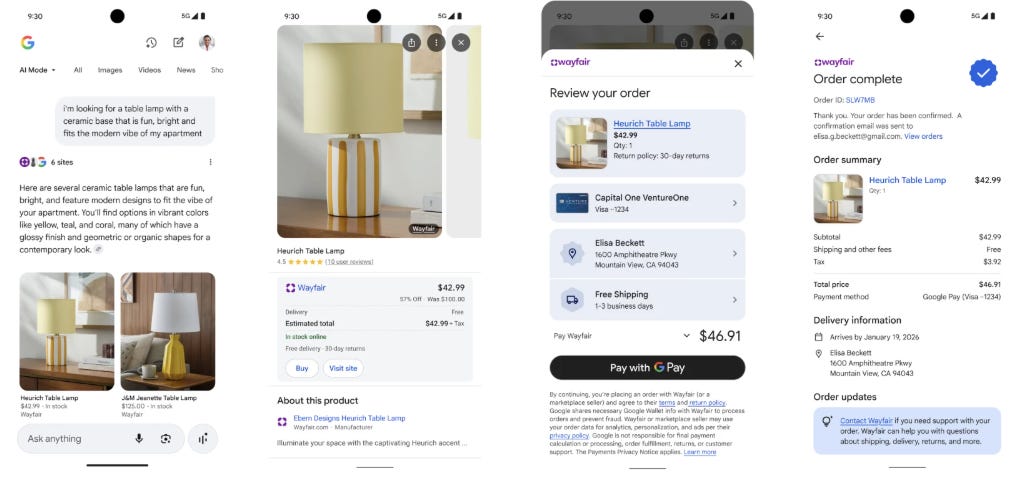

Google’s AI Mode Shopping Experience with Wayfair

Source: Google

When most people imagine agentic commerce, they picture something more expansive: a consumer gives an initial set of instructions and an agent handles the entire discovery and transaction process with minimal human interaction, coordinating directly with merchant agents to complete the purchase. Platforms like OpenClaw are providing early signals of what this could look like — both the promise and the risks, with legitimate security concerns already surfacing. But if history is a guide, that hypothesized end-state is likely years away, at least for certain categories. Even if adoption accelerates, the impact on the broader retail and ecommerce landscape will likely be iterative rather than existential for existing players. After two-and-a-half decades, ecommerce is still less than 20% of total retail sales and the most powerful paradigm shift in ecommerce – mobile – accounts for less than 50% of all ecommerce transactions, nearly two decades after the iPhone was launched.2 If agentic follows a similar adoption curve, it becomes another channel merchants must plan for alongside in-store, desktop, and mobile.

There are a few trajectories agentic could take:

AI reduces friction within the existing checkout flow — auto-filling personal and payment information — showing up as higher conversion rates with no material structural change to the underlying experience.

LLMs improve the discovery layer without replacing the transaction. Instead of searching separately for hotels and flights, a consumer inputs travel dates and destination, and the LLM assembles a potential itinerary.

Agents go beyond discovery and handle price comparison and review aggregation, filling the checkout basket while the consumer retains final approval over payment.

Agents handle the entire end-to-end purchase process with little-to-no human input — the scenario most likely to emerge if personalized agents gain broader traction.

Even short of a fully agentic experience, AI’s impact on ecommerce fundamentals could be substantial. Cart abandonment remains structurally high at ~77% globally.3 The conversion rate for the average ecommerce transaction sits under 3% — with some categories closer to 1% — meaning the overwhelming majority of visitors never complete a purchase.4 Ecommerce return rates run over 19%.5 Better product matching and predictive analytics have clear roles to play in all three even without an agent handling the entire commerce journey.

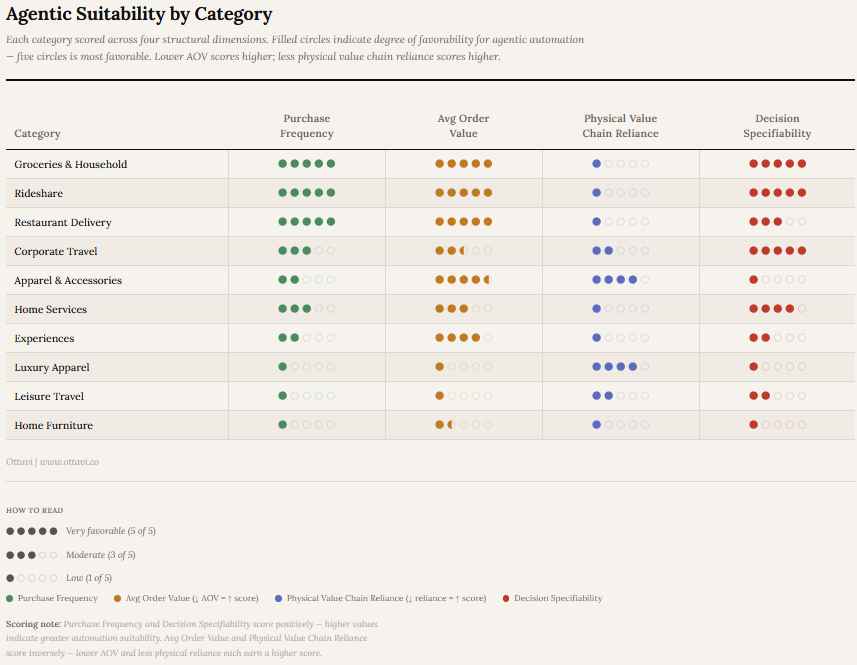

Agentic Suitability: Shopping Friction

Understanding how far into the purchase funnel agents will go — or more accurately, how far their human will allow them to go — depends in large part on the friction in the shopping process. A useful lens is to evaluate consumer categories across four criteria:

Purchase Frequency measures how often a consumer buys within a given category. Higher frequency gives an agent more opportunities to learn preferences, but it also deepens loyalty to the platform or retailer delivering the product — which can actually reduce reliance on a third-party LLM as the interface.

Average Order Value reflects the average dollar amount per transaction and serves as a reasonable proxy for per-transaction decision stakes and consumer risk tolerance. The higher the AOV, the more likely the consumer wants to be consulted before purchasing.

Physical Value Chain Reliance captures how much of the customer value proposition depends on real-world logistics, discovery, or in-person fulfillment. The more the experience lives in the physical world, the less likely agents are to own the end-to-end process. An LLM can aggregate supply — but can it deliver as quickly, cheaply, and reliably as Amazon or DoorDash?

Decision Specifiability is perhaps the most important and underappreciated criterion: the degree to which a consumer’s purchase preferences can be fully expressed as objective, machine-readable parameters before the transaction occurs. A decision that can be parameterized has a far higher probability of being delegated to an agent than one that relies on aesthetic judgment or subjective evaluation. Reordering the same grocery list weekly sits at one end of this spectrum; selecting a piece of jewelry sits at the other.

*The above examples are meant to be illustrative.

Categories with low purchase frequency and high AOV — a vacation to Thailand, say — present a specific set of dynamics. The infrequency makes it hard for brands or platforms to build loyal repeat relationships, while the stakes make consumers want to shop around, price compare, and retain final approval. These categories are natural candidates to replace traditional search with conversational LLM-based discovery, but they are unlikely to become fully agentic. The discovery layer will probably be agent-led; the final decision, including payment confirmation, will remain human (think of this as “human-aided agentic”).

However, this likely won’t be the case for all travel. The frequent business traveler who books the same hotel every week is highly likely to have their agent — or Hilton’s in-app agent — handle the booking directly, with a card on file and Hilton Honors rewards intact. One scenario involves infrequent, high-stakes friction. The other involves frequency with almost none.

High-frequency, low-AOV categories appear best suited for a fully agentic experience. But these are also the categories where dominant retailers and marketplaces are best positioned to own the customer relationship precisely because of that frequency. If you order groceries from Amazon every week, you’re starting your journey in Amazon — not in ChatGPT or Gemini or Claude. If you order from your favorite local taco spot through DoorDash every Friday, you’re going back to DoorDash. For these categories, Amazon’s Rufus or DoorDash’s native agent is far better positioned to own the interface than a general-purpose LLM. This is agentic commerce — just not the version most people are imagining, and far less disruptive to incumbents than the headlines suggest. Here, LLMs function more as a new customer acquisition channel, structurally analogous to Google search or paid social.

These categories also tend to have material physical-world components that are critical to the customer experience. The degree to which this matters depends on whether the incumbent actually owns that physical experience. DoorDash’s delivery network is a structural differentiator because DoorDash controls it end-to-end. The lodging experience from a hotel booked on Booking.com, by contrast, is non-exclusive to Booking and largely separate in the consumer’s mind — making the physical world less of a structural advantage for Booking, even though the stay itself is central to why the customer booked in the first place.

Media subscriptions — Netflix, Spotify — represent a distinct case worth noting. The subscription model effectively internalizes the discovery problem rather than outsourcing it to an LLM, which insulates these platforms from third-party agent disruption at the top of the funnel. Their opportunity lies in building proprietary in-platform agents that improve content discovery within a walled ecosystem.

Will Agentic Commoditize Marketplaces?

The core value proposition for most marketplaces is reducing search costs through supply aggregation. Given how LLMs work, it’s worth asking whether certain marketplaces become commoditized over time — specifically those whose value is concentrated in discovery rather than physical execution. Travel will likely be one of the first categories where this theory is tested. That’s not coincidental — travel was among the first verticals to move online, precisely because the product is inherently digital at the point of discovery: you research, compare, and book well in advance of “consumption” (i.e., the stay).

Booking.com and Expedia dominate US online travel, including hotels. Their respective moats today are supply-side scale and continuous iteration on the discovery and checkout experience, which yields conversion advantages that they reinvest into supply acquisition and demand generation. Booking.com, in particular, has managed the Google ecosystem better than perhaps any other marketplace and is one of Google’s largest advertisers. But in a world where hoteliers are actively standardizing for agentic connectivity — APIs, structured data, direct feeds — does the value of supply aggregation start to erode? Specifically, if agents are sourcing the best inventory on criteria — pricing, reviews, proximity to destination, etc. — does this neutralize the advantages that have been created through supply aggregation (i.e., historically built through performance marketing and conversion optimization)?

Booking’s CEO Glenn Fogel addressed this directly on a recent earnings call:

“Look, we’ve been competing, so to speak, with a top-of-the-funnel player who’s very big for a very long time and people go there, but yet then they come to us direct many of them. Why? Because we are offering them something of value. That’s what I believe is going to continue. And by the way, it’s been very successful for that large person at the top of the funnel, Google. We’ve both done very well. They’ve made very good money setting up an auction format for taking advertising, and we have been more than happy to pay a lot of money as have competitors of us. It’s worked out really well for them. It’s worked out really well for us. And by the way, some of these other large language models when they’re looking at this, they may say, that’s the right way to do it. Not go down the funnel, don’t become a merchant of record, take it high above, don’t deal with the mess of the day-to-day in and out that we have to deal with all the time, successful for us, successful for them. I think that’s the way it’s probably going to go in the end, but that’s my opinion.”

Fogel’s broader point — that LLMs will likely monetize at the top of the funnel through an advertising model, much as Google has, rather than competing downstream in the complexity of payments and operations — is reasonable and probably correct. Google’s own history with travel OTAs is the proof of concept: it built an enormously profitable business sitting above the transaction, never becoming a merchant of record itself. However, depending on how agents source and rank inventory, it could result in more hotels going direct — cutting out middlemen like Booking.

Wyndham discussed its efforts on its Q4 call this week:

“We continue to work with public LLMs, including Google AI Mode and ChatGPT, to establish direct connections of our hotel data to eliminate the need for these models to scrape our sites. In November, Google selected Wyndham as one of a handful of partners to take part in an agentic booking experience on AI Mode in search. Soon, guests will be able to discover Wyndham properties through natural conversational interactions while our connected systems enable seamless direct bookings within AI Mode. We’ve also successfully connected to Anthropic’s Claude.”

Fogel cited being the merchant of record and handling payments as a key advantage:

“You want to be merchant of record, payments — that’s really complex. We have over 100 different payment methods, more than 50 currencies... regulations on the payment here is tremendous... You want to be involved in the travel business and you want to be dealing with merchant of record... that’s just the EU. And then, of course, the national regulations — we’re dealing with over 200 countries... Do we think that the large language models are going to be entering and want to enter down the funnel down to where we are? I don’t think so.”

I agree with Fogel that LLMs are unlikely to go deep into the funnel and participate after the transaction, but supply aggregation as an advantage is likely to diminish over time, especially as hotels modernize their infrastructure and establish direct feeds to LLMs. Today, Booking’s access to over four million properties — particularly independents running outdated property management systems — is genuinely hard to replicate. The long tail of independent hotels will take years to convert; however, the top six hotel chains already account for nearly 60% of US hotel rooms, and they are moving quickly.6 This doesn’t mean Booking and Expedia disappear. But their value proposition gradually shifts. If their differentiation shifts down the value chain — from discovery and demand generation toward payments infrastructure and customer service — the result is likely take rate compression. The typical marketplace captures 15-25% of the transaction value versus 3-6% for merchant-of-record / payment providers.

This dynamic is likely to play out across categories: agents will go as far into the funnel as friction, stakes, and specifiability allow. In the near term, the clearest winners are incumbents who own frequency and the real-world part of the value chain. The ones who are most at risk are those who rely on differentiating through discovery where LLMs can erode their current supply aggregation advantages.

The Information.

US Census Bureau, eMarketer.

Dynamic Yield.

Dynamic Yield.

National Retail Federation. “2025 Retail Returns Landscape.”

Marriott, Hilton, Choice, Hyatt, Wyndham, IHG Public company filings, STR.