US Travel Trends: November 2025 Update

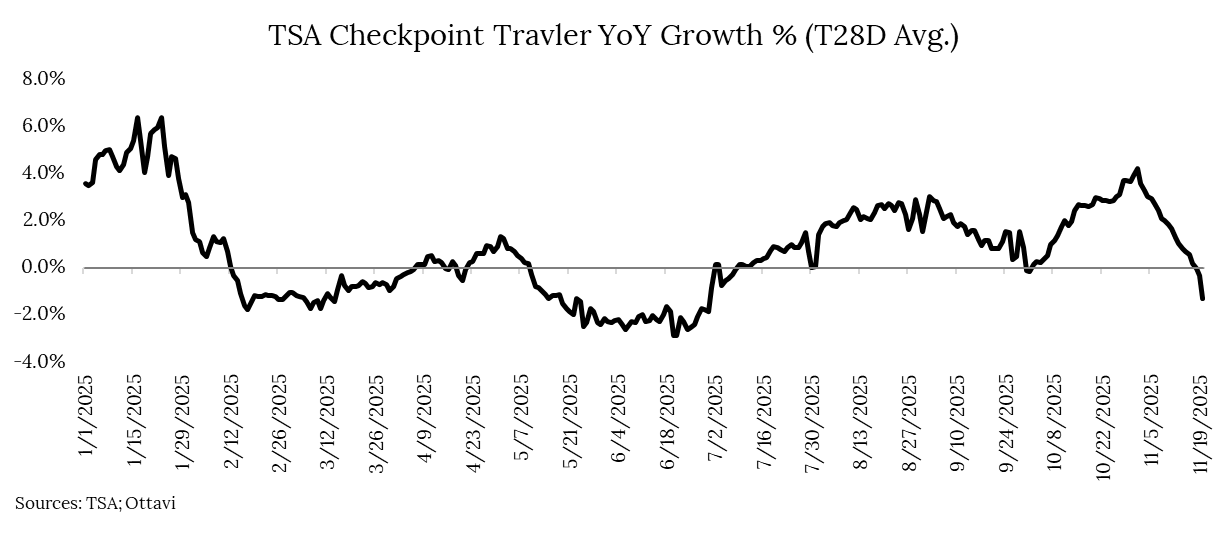

Recap: Travel demand has seesawed in 2025—firming through summer and early fall before slipping again in recent weeks. This is likely due to the government shutdown, not a structural slowdown. Beneath the surface, however, a stark divide persists: affluent travelers continue to spend, while budget-conscious consumers and foreign visitors—especially Canadians—are pulling back.

As written in June, travel demand showed signs of softness heading into the summer. It strengthened steadily through July and August and accelerated after Labor Day as the U.S. entered the peak corporate travel season. Recently, this momentum has reversed, with the trailing 28-day average turning negative year-over-year. This dip is likely tied to flight-capacity reductions stemming from the government shutdown rather than a true demand deterioration. If that’s the case, TSA throughput should rebound in the coming weeks as the holiday travel season ramps up.

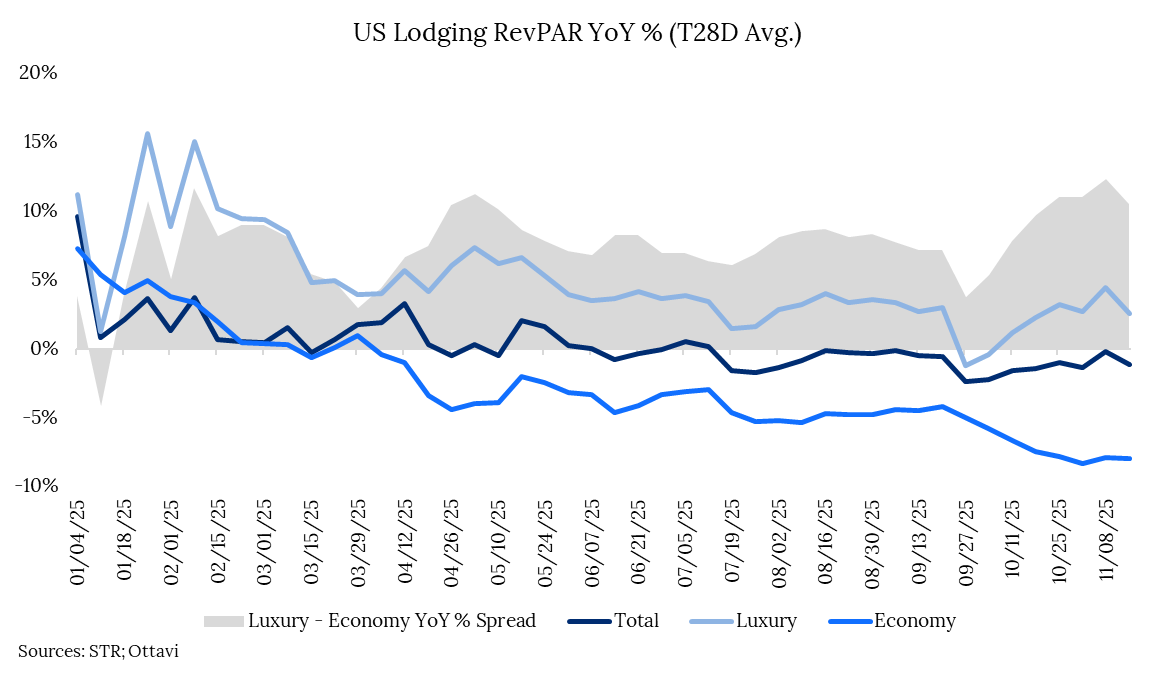

Assuming this recent weakness proves transitory, the rebound since July has been far from broad-based. The U.S. economy continues to display a “K-shaped” pattern: higher-income consumers are spending freely, buoyed by rising wages and wealth effects from strong equity markets, while lower-income households remain pressured by persistent inflation and stagnant real wage growth. This divide is clearly visible in the hotel sector.

Across the industry, U.S. revenue per available room (RevPAR) has hovered within a narrow –1% to +1% range for much of the year. But performance at the ends of the price spectrum has sharply diverged. Luxury hotels have posted roughly 5% RevPAR growth in 2025, while Economy properties are down about 3%—an 8-point gap. That spread has widened to 11 points more recently as Economy demand has continued to deteriorate. For context, the Luxury–Economy gap averaged just 2 points from 2010 through February 2020. Economy hotels have not generated year-over-year growth since March—33 consecutive weeks of contraction.

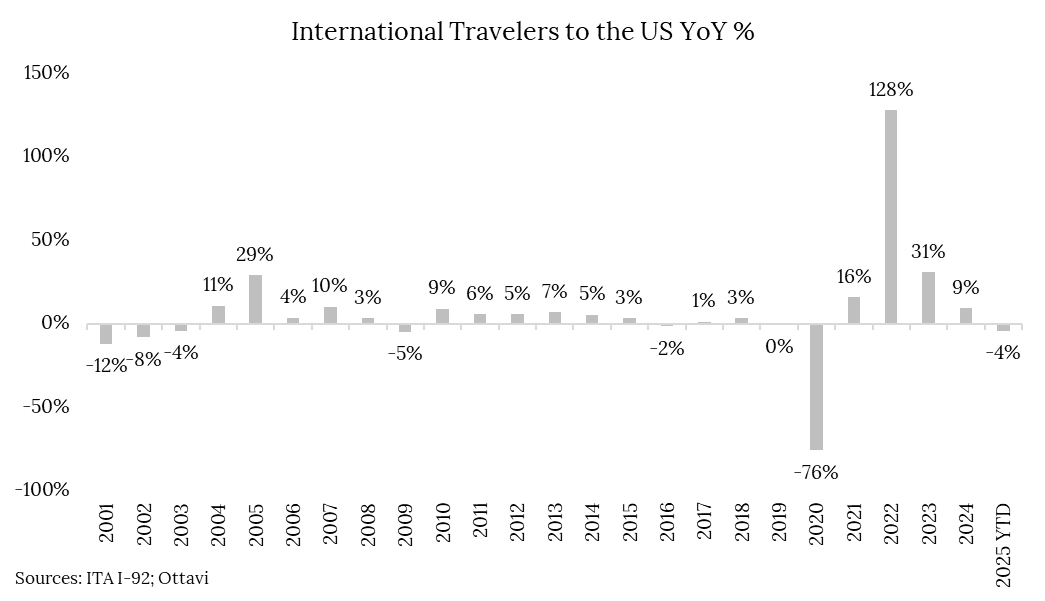

International travel has also weighed on overall demand in 2025, though its impact is smaller given foreign visitors represent only a mid-single-digit share of total trips. Total foreign arrivals are down 4% year over year, driven largely by a sharp pullback from Canadians. Statistics Canada reports that return trips to the U.S. from February to October fell 21% by air and 34% by car. Canadians accounted for roughly a quarter of all foreign visitors to the U.S. in 2024, making them responsible for much of the inbound decline. Notably, foreign travel to the U.S. rarely contracts outside of economic downturns.