What CLARITY Means for CRCL/COIN; Tether's Audit

A lot is happening in stablecoin land today. The CLARITY Act market structure bill is seemingly close to being finalized and Tether is moving forward with a “Big Four” audit. Circle (CRCL) and Coinbase (COIN) stocks declined 20% and 10%, respectively.

CLARITY Act

Below is a good summary of what’s happening behind the scenes from Crypto in America’s Eleanor Terrett:

According to an internal stakeholder email shared with me, the proposal would prohibit platforms from offering yield “directly or indirectly” for holding a stablecoin or in a manner that resembles a bank deposit. The restriction would apply broadly to digital asset service providers (exchanges, brokers, etc.) and their affiliates to limit workarounds, and would bar anything “economically or functionally equivalent” to interest.

The proposal would also permit activity-based rewards tied to user activity, including loyalty, promotional, or subscription programs, provided they are not deemed economically or functionally equivalent to interest. It would also direct the SEC, CFTC, and US Treasury to jointly define permissible rewards and establish anti-evasion rules within one year.

If passed, prohibiting offering yield “directly or indirectly” would seemingly end the “rewards” workaround CRCL/COIN have been using to pass yield from CRCL → COIN → end users. And barring anything “economically or functionally equivalent” to interest is purposefully vague and broad. The bill delegates enforcement to a joint SEC/CFTC/Treasury rulemaking within 12 months, meaning the actual boundaries won’t be known until well after the bill passes.

Either way, COIN’s current rewards program for purely holding USDC appears to be squarely in the crosshairs. I’m sure COIN is working on a structure that wouldn’t be classified as sharing interest, but that structure is TBD and the likelihood of success is unknown.

In Q4, CRCL generated $770M in revenue, of which $733M (or 95%) was “Reserve Income” — revenue generated from the interest earned on USDC reserves. CRCL shares this yield with partners like COIN and Binance through distribution partnerships. In total, CRCL passed through 63% of its Reserve Income — and 60% of its total revenue — to distribution partners, retaining the remaining 37%. This is essentially CRCL’s gross profit.

COIN captures the lion’s share of the pass-through, receiving ~50% of CRCL’s Reserve Income. COIN then uses some of these fees (which it recognizes as Stablecoin Revenue) to incentivize Coinbase One subscribers, offering 3.5% APY on USDC balances. In Q4, COIN reported that it spent ~35% of its Stablecoin Revenue on what it calls “USDC Rewards” — $127M out of $364M in Stablecoin Revenue.

Immediate Implications

For CRCL: There’s no change to its current distribution agreements with COIN and others, so its Net Reserve Margin should stay the same.

For COIN: It will still collect ~50% of CRCL’s Reserve Income as Stablecoin Revenue. However, it will need to rethink how it passes USDC Rewards through to end users and Coinbase One subscribers. If COIN stops rewards altogether, this could increase near-term profitability. Had the $127M in Q4 USDC Rewards gone away entirely, adjusted EBITDA would have increased 23% to $693M. (COIN CEO Brian Armstrong himself has publicly acknowledged that a yield ban would make COIN more profitable short-term)

Mid-Term Implications

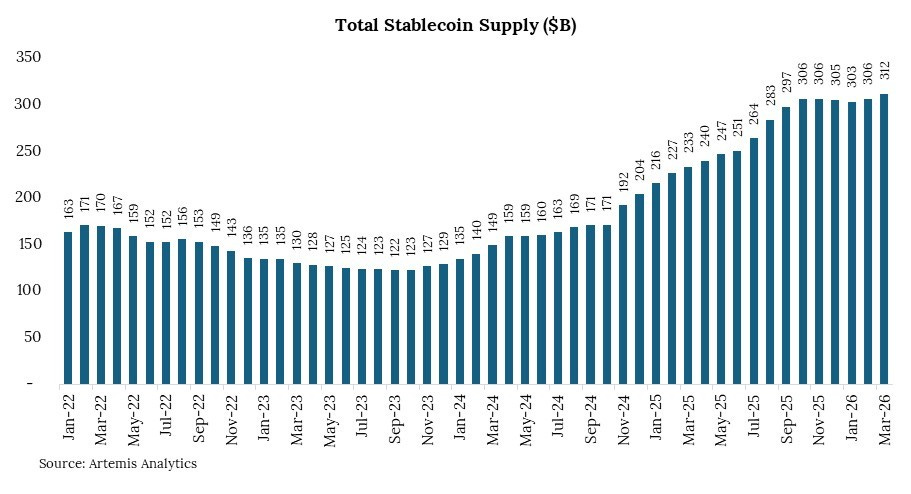

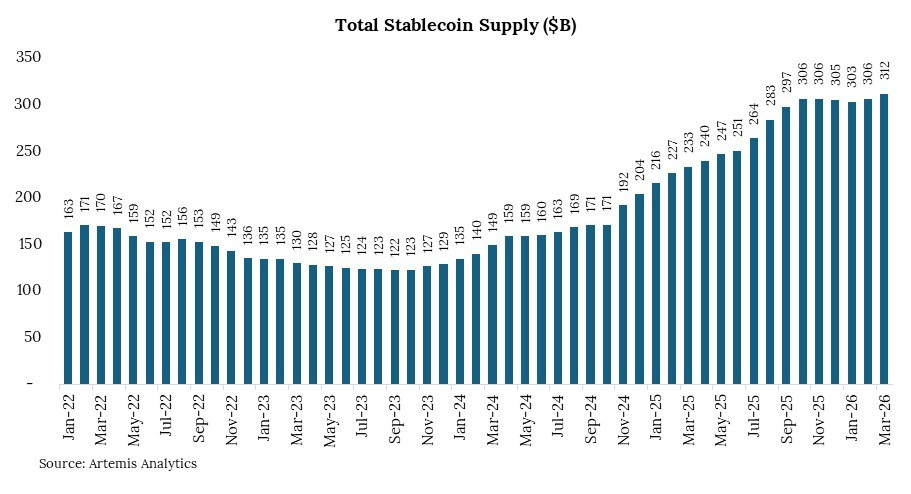

For USDC holders in the US and other developed markets, receiving no rewards from COIN and others makes the stablecoin less valuable, which could slow the growth in stablecoin supply. In emerging markets, holding the dollar still has value without being paid yield. Total stablecoins are up 34% year-over-year but only up ~2% since October. A further slowdown in growth would directly and negatively impact CRCL and COIN revenue.

For COIN, being prohibited from offering USDC yield reduces the core value proposition of Coinbase One. If COIN cannot find a comparable way to incentivize subscribers, it could see slower sub growth and associated trading volume and revenue. The permitted activity-based carveout (payments cashback, trading fee rebates, DeFi lending on Base) offers a path forward, but none of those individually replaces the simplicity of “hold USDC, earn 3.5%.”

This also calls into question how the terms of future distribution agreements might be affected. If COIN can no longer pay USDC rewards, is CRCL willing to give up ~50% of its Reserve Income? That will seemingly depend on whether COIN can find a workaround to pay "rewards" within the confines of the law.

Long-Term Implications: US Payments Disruption Case More Challenging

The more interesting longer-term question is how this impacts the case for stablecoins to disrupt traditional card-based payments. I've been skeptical stablecoins would disrupt Visa or Mastercard anytime soon; however, one potential disruption scenario would be to use rewards to encourage consumer stablecoin adoption and essentially create a better debit alternative by passing at least a portion of reserve yield through to the consumer via transaction-based rewards (similar to cashback).

Stablecoins are at a competitive disadvantage versus credit cards given the same interchange-based model those in favor of stablecoins deride provides variable unit economics (i.e., the 2-3% per transaction) to fund rewards and issue credit. However, this is not the case for debit — largely due to the Durbin Amendment capping interchange for large issuers at $0.21 + 5 basis points of the purchase value. This could in theory allow a stablecoin-based incentive mechanism that is unlikely to match traditional credit cards but would be an improvement over debit.

The challenge is that even this path requires using balance-based revenue (reserve income) to fund activity-based rewards — which may still fall in the gray zone of the CLARITY Act's "economic equivalence" standard. And prohibiting yield sharing more broadly removes the most plausible mechanism for getting stablecoins into consumer wallets at the scale needed to make any of this work. Without widespread adoption, the front-end disruption case likely stalls. What does seem likely is that for consumer-based payments in the US, stablecoins will be relegated to better back-end settlement infrastructure — a role Visa, Mastercard, and Stripe are already co-opting — rather than a disruptive front-end payment method.

On Tether

Separately, Tether announced it is undergoing a Big Four audit (though it didn’t name the auditor). I think CRCL’s selloff is at least in part due to this news and the expectation that it could signal increased competition from Tether’s USDT. This is less about US competitive dynamics and more about international ones.

Tether’s GENIUS Act-compliant stablecoin, USAT, has gained little traction since launching in January. USAT’s market cap is currently ~$20M vs. USDT’s $184B and USDC’s $81B. USDT is ~64% of total global stablecoin supply; USDC is ~28%.

Tether’s issues with US regulators are well documented — the $41M CFTC fine, the $18.5M NYAG settlement, and the reported DOJ probe into sanctions and AML violations. But Tether, for all its dominance globally, has run into obstacles with foreign regulators as well. Tether did not pursue MiCA compliance in the EU, resulting in USDT being delisted from every major European exchange — Binance, Kraken, Crypto.com, Bitstamp, OKX — between January and March 2025. CRCL, by contrast, is fully MiCA-compliant through its French EMI license. Same story in Japan, where USDC was the first foreign stablecoin permitted by the FSA.

An audit is a long way from regulatory compliance. But if it signals that Tether is moving in that direction, it at least raises the question of increased competition with CRCL in the regulated international markets where USDC has been gaining share precisely because of Tether’s compliance gaps.

Obvioulsy there was a spurt of growth post GENIUS and I think the recent flatter growth had some idiosyncratic issues but the bull case is that agents will use stablecoins. That said when you think about a country such as Argentina which held $200bn in actual cash USD, they have replaced 60% of that with stablecoins already, and there are fintechs helping them spend it as necessary at local merchants. These merchants get fiat. However how many more Argentina’s are there, Bolivia etc - it’s a finite amount of money. So if you assume these countries already adopted it quite a bit you can’t assume that rate of growth from that source is sustainable. When it comes to use cases up against credit cards in more mature countries - sometimes tech bros in particular are not as familiar with longstanding principals such that it is the consumer who chooses how to pay, and stablecoin doesn’t give you typical consumer anything. You have recourse to Visa if the product you buy is defective or a fruad - not so with stablecoin as yet. I’m sceptical that stablecoin can grow to be massive as that would assume some countries ttaly give up sovereingty over their currency and so they could tax stable transactions to control the growth if that’s a concern. The other thing to note is that there’s a ton of new laws impacting the space - esspecially the reporting such as idenification of both sender and reciever - that takes away some advantage certain people were using to evade taxation etc. So yes it’s going to be a growth market but prudence would require that most enterprises don’t keep a lot tied up at Circle etc regardless of what is backing it as your counterparty is not Uncle Sam but a private company that’s not exactly JP Morgan. As such even before the recent news I was always sceptical of those trillions expectations.